Trader Hub

Sheng Siong Group Ltd – Seasonal and Base Effect Bump

traderhub8

Publish date: Mon, 29 Apr 2024, 10:20 AM

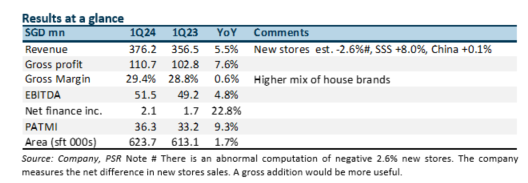

- 1Q24 revenue and PATMI were within expectations at 26%/26% of our FY24e forecast. Same-store sales growth accelerated to 3.6% benefitting from the later lunar new year.

- Only one new HDB store was secured in 1Q24. The pipeline is healthy with three stores tenders submitted and another six to be tendered out. The lack of new stores will keep growth muted this year.

- We maintain our FY24e forecast and target price of S$1.66. Our valuations are based on historical PE of 18x. Only two stores were opened last year. The lack of new stores will be a drag on revenue this year. With industry-leading margins, it will be challenging for Sheng Siong to expand further. Supply chain bottlenecks include distribution centres. Another avenue for growth is acquisitions, as the company has built up a record net cash hoard of S$352 million.

The Positive

+ Acceleration in revenue and margins. Same-store sales jumped 8% (effective growth from 63 matured stores is 3.6%). This year, the longer days between Christmas and Lunar New Year provided an additional runway for festive shopping. It was much closer last year, where shopper fatigue can occur. Margins were supported by higher house brand sales, especially the successful rollout of frozen products.

The Negative

– Only one new store was secured this year. Only one new store opened this quarter in Clementi. A positive has been the narrowing number of bidders for the stores. There are now typically three bidders for stores compared to four or five in the past.

Source: Phillip Capital Research - 29 Apr 2024

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

SASSEUR REIT – FY24e Sales Will be Driven by Promotional Events

Created by traderhub8 | May 15, 2024

ST Engineering Ltd – All Engines Roaring, But Satellite No Signal

Created by traderhub8 | May 14, 2024

Memiontec Holdings Ltd. – Fully Integrated Water Infrastructure Provider

Created by traderhub8 | May 13, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Apps

Top Articles

1

Trader Hub

2

RHB Investment Research Reports

ComfortDelGro - Seasonally Weak 1Q24; Better 2H24 Expected; BUY

4

RHB Investment Research Reports

Thai Beverage - Beer Segment Supporting Outlook; Maintain BUY

5

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....