Trader Hub

Thai Beverage PLC – Waiting for Macro to Turnaround

traderhub8

Publish date: Fri, 24 Nov 2023, 11:17 AM

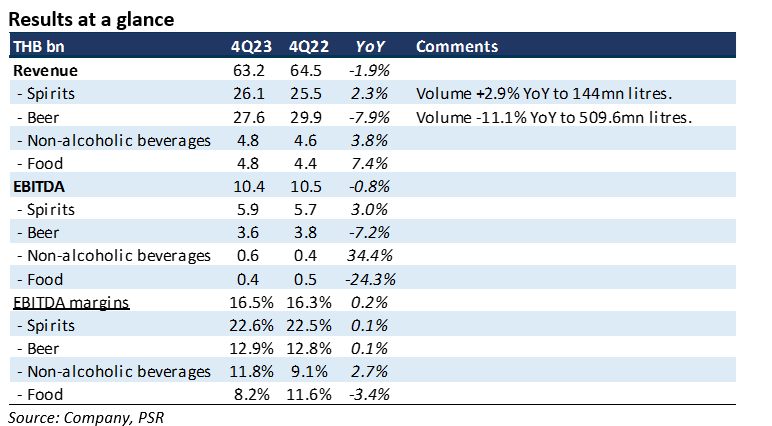

- Results were marginally below expectations. 2023 revenue and PATMI were at 97%/95% of our FY23e forecasts. Beer revenue and associate earnings were below our estimates.

- Spirits EBITDA grew 3% YoY in 4Q23 to THB5.9bn due to growth in volumes. Beer EBITDA fell 7% to THB3.6bn, as beer volumes declined by 11%, the third consecutive quarter of contraction.

- We lower our FY24e PATMI by 9%. Beer is facing soft consumer demand in Vietnam due to the weak economic conditions, and made worse by five cumulative rounds of price increases since 2021. In Thailand, the emergence of Carabao as a new beer competitor further raised the pricing and marketing intensity. We expect growth in spirits revenue from normalisation of white spirits volume, price increases and higher mix of brown spirits. More aggressive fiscal spending in Thailand next year will support consumption spending. Our BUY recommendation is maintained but target price is lowered from S$0.75 to S$0.67. We roll-over valuation to FY24e earning but PE ratio is lowered to the 3-year average of 16x (prev. 18x). The listed associates are valued at 20% discount to current market price.

The Positive

+ Resilient spirits volume. Spirit volume expanded 2.9% YoY to 114mn litres from higher demand of the more expensive brown spirits. The brown spirits share of volume is still below pre-pandemic levels. White spirits volume were softer due to front loading a year ago.

The Negative

– Beer still suffering. Both beer revenue and EBITDA declined around 7%. Volumes contracted a larger 11% as a cumulative round of price increases has hurt consumption that is already weak from the soft macro environment, particularly in Vietnam.

Source: Phillip Capital Research - 24 Nov 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Trader Hub

Singapore REITs Monthly: April24 – Pricing in Higher-for-longer Interest Rates

Created by traderhub8 | May 20, 2024

SASSEUR REIT – FY24e Sales Will be Driven by Promotional Events

Created by traderhub8 | May 15, 2024

ST Engineering Ltd – All Engines Roaring, But Satellite No Signal

Created by traderhub8 | May 14, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Apps

Top Articles

1

2

CEO Morning Brief

Singapore Air Staff Get Eight Months' Salary Bonus After Record Profits

3

CEO Morning Brief

Singapore's First New PM in 20 Years Holds Inaugural Cabinet Meeting

4

Trader Hub

5

RHB Investment Research Reports

ComfortDelGro - Seasonally Weak 1Q24; Better 2H24 Expected; BUY

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....