Trader Hub

Venture Corporation Limited – as Weak as During the Pandemic

traderhub8

Publish date: Mon, 06 Nov 2023, 11:45 AM

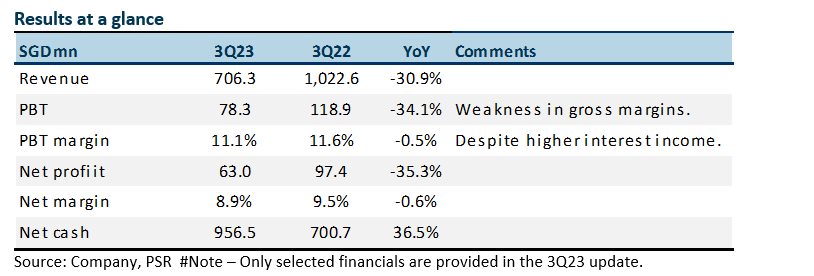

- 3Q23 PAT was down 35% YoY to S$63mn. The results were below expectations. 9M23 revenue and PAT were 70%/69% of our FY23e forecast. Soft demand and inventory adjustment continue to weigh down on revenue and earnings.

- The pace of decline should narrow in 4Q23e as contributions from new product introductions and supply chains transition from China to SE Asia.

- We cut our FY23e revenue and PATMI by 7% and 8%, respectively. We maintain our NEUTRAL recommendation. Our target price is lowered to S$12.50 (prev. S$15.20) due to our cut in earnings and a reduction in our PE ratio to 13x (prev. 15x). Venture’s valuation continued to de-rate as growth has stuttered over the past five years. The dividend yield of 6% is attractive and sustainable with its cash hoard of S$956mn.

The Positive

+ Recovery in net cash. Net cash recovered by S$255mn YoY in 3Q23 to S$956mn. Inventory declined by S$304mn YoY to a still elevated S$949mn. Inventory is high compared to pre-pandemic levels of around S$700mn.

The Negatives

– Weakness in margins. There was no disclosure of gross margins this quarter. But assuming interest income was similar to prior quarters, operating margins declined by at least 1% point. This was despite staff costs declining around 9% YoY.

– Revenue slump. Revenue growth remains problematic for Venture. 3Q23 revenue of S$706mn is trending around supply chain pandemic levels.

Source: Phillip Capital Research - 6 Nov 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Trader Hub

Singapore REITs Monthly: April24 – Pricing in Higher-for-longer Interest Rates

Created by traderhub8 | May 20, 2024

SASSEUR REIT – FY24e Sales Will be Driven by Promotional Events

Created by traderhub8 | May 15, 2024

ST Engineering Ltd – All Engines Roaring, But Satellite No Signal

Created by traderhub8 | May 14, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Apps

Top Articles

1

2

CEO Morning Brief

Singapore Air Staff Get Eight Months' Salary Bonus After Record Profits

3

CEO Morning Brief

Singapore's First New PM in 20 Years Holds Inaugural Cabinet Meeting

4

Trader Hub

5

RHB Investment Research Reports

ComfortDelGro - Seasonally Weak 1Q24; Better 2H24 Expected; BUY

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....