Trader Hub

Venture Corporation Limited – No Recovery Visible, Only Dividends

traderhub8

Publish date: Mon, 07 Aug 2023, 11:26 AM

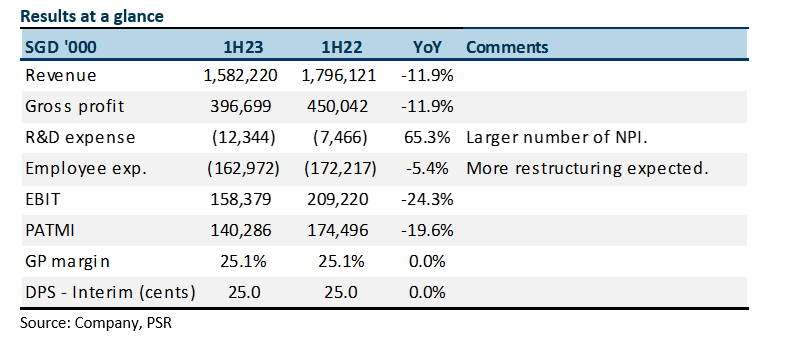

- 2Q23 PAT was down 26% YoY to S$66.7mn. Results were below expectations. Revenue and PAT were 44%/45% of our FY23e forecast. Medical devices demand is down post-pandemic and other electronic products face overstocking. Interim dividend is maintained at 25 cents.

- We expect the weakness in revenue to persist until year-end. Recovery will come from new products such as EV chargers, semiconductor equipment and data centres.

- We lower our FY23e PATMI by 5% to S$296mn. Our revenue estimates are cut by 8% to S$3.3bn. We maintain our NEUTRAL recommendation. Valuations and dividend yield of 5.2% have turned more attractive, but there is little visibility of a recovery in the near-term. The target price is lowered to S$15.20 (prev. S$17.10), 15x PE FY23e. Our target valuations have been lowered as current earnings have a higher composition of interest income (7% vs 2% historically).

The Positive

+ Stable gross margins and healthy net cash. Despite the weaker revenue, gross margins were stable at 25.1%. We believe the weaker ringgit, lower freight cost and reduced labour force were some of the drivers to stable margins. Net cash improved by S$191mn YoY to S$896mn. The cash hoard has turned interest income into an earnings growth driver. 1H23 interest income jumped 4-fold from S$3.1mn to S$12.5mn.

The Negative

– Inventory is still too high. Inventory in 1H23 declined by S$248mn to S$1,002mn. With the lower revenue run-rate, inventory remains a concern with the possibility of write-offs, in our opinion. Annualised inventory days are currently around 137 days vs the pre-pandemic average of 100 days. This implies an excess of almost S$250mn of inventory compared to the historical average.

Outlook

We expect weakness to persist into the third quarter. The foundation of future growth for Venture stem from new programmes and customers looking to de-risk their supply chain out of North Asia into SE Asia. Malaysia is an attractive location for the deepening scale of the supply chain, skill sets, available space, and low-cost production. Singapore complements engineering expertise and oversight.

Source: Phillip Capital Research - 7 Aug 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Trader Hub

Singapore REITs Monthly: April24 – Pricing in Higher-for-longer Interest Rates

Created by traderhub8 | May 20, 2024

SASSEUR REIT – FY24e Sales Will be Driven by Promotional Events

Created by traderhub8 | May 15, 2024

ST Engineering Ltd – All Engines Roaring, But Satellite No Signal

Created by traderhub8 | May 14, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Apps

Top Articles

1

2

CEO Morning Brief

Singapore Air Staff Get Eight Months' Salary Bonus After Record Profits

3

CEO Morning Brief

Singapore's First New PM in 20 Years Holds Inaugural Cabinet Meeting

4

Trader Hub

5

RHB Investment Research Reports

ComfortDelGro - Seasonally Weak 1Q24; Better 2H24 Expected; BUY

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....