Trader Hub

Sheng Siong Group Ltd – Lack of New Stores

traderhub8

Publish date: Fri, 01 Mar 2024, 10:44 AM

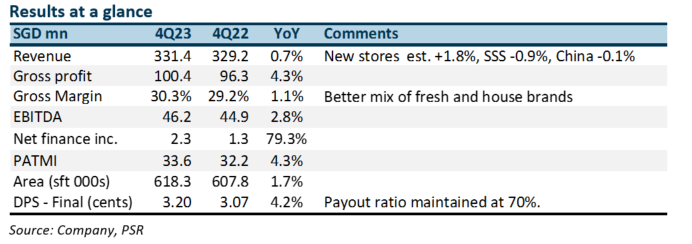

- FY23 revenue and PATMI were within expectations at 99%/99% of our forecast. Revenue growth was 2.1% YoY. Same-store sales contracted and new-store expansion was muted.

- For 2023, Sheng Siong only expanded with two new stores or a footprint growth of 1.7% (2022: +5.4%). The lack of new stores will weigh on revenue growth this year. The company aims to expand a minimum of three stores or equivalent 2.4% expansion per year.

- Same-store sales growth is expected to improve as outbound travel normalises. Inflationary pressure will also support more dining at home. The company has secured two stores so far this year in Singapore, with another ten likely to be tendered. We marginally lower our FY24e earnings by 2%. With a more sluggish growth outlook, we lower our target valuations from historical 20x PE to 18x. The target price is reduced to S$1.66 (prev. S$1.80). Until new stores accelerate, growth will be muted.

The Positives

+ Rise and rise of margins. Gross margins have been on an upward trajectory since listing. A decade ago, gross margins were 23% in FY13 and now stand at 30%. Scale, distribution centre, direct sourcing, and fresh food mix have been the major driver of margin expansion. The new driver is house brands. Competitors have also been raising prices to pass on their cost of production.

The Negatives

– No new stores. There were no new stores this quarter, and only two were opened this year. Expansion in new stores is a cumulative 8% over three years. Before this lull, new stores grew 7-8% p.a. The lack of new stores was due to fewer tenders made available. Of the five stores tendering in 2023, Sheng Siong has been successful in securing three.

Source: Phillip Capital Research - 1 Mar 2024

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Singapore Telecommunications Ltd – Down Under Is Turning Around

Created by traderhub8 | May 27, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Apps

Top Articles

1

SGX Market Dialogues

10 in 10 With NetLink NBN Trust - The Fibre of a Smart Nation

2

SGX Market Updates

3

CEO Morning Brief

Singapore Airlines’ CEO Gets Pay Jump After Record Annual Profit

4

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....