Trader Hub

Lendlease Global Commercial REIT – High Rental Reversion and Rental Upside From Sky Complex

traderhub8

Publish date: Mon, 05 Feb 2024, 10:01 AM

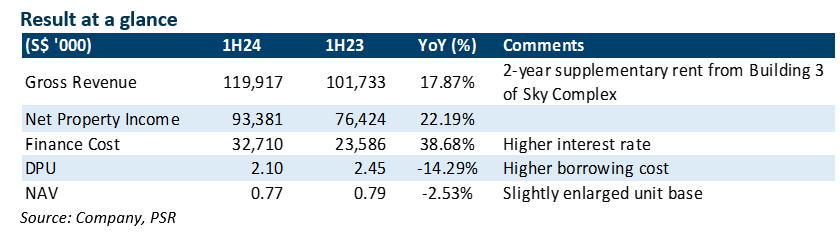

- Gross revenue increased by 17.9% to S$9mn with the 2-year supplementary rental from Building 3 of Sky Complex and form 55% of our FY24e forecast.

- NPI increased 22.2% YoY while DPU slid 14.5% YoY to 2.1 cents, and were 54%/52% of our FY24e estimates. High rental reversion was sustained with 313@somerset at c.20%, and Jem provided a stable contribution at c.10%.

- We reiterate our BUY recommendation with lower DDM-TP of S$0.83 and FY24e-25e DPU forecast of 4.16-4.59 Singapore cents. Erosion of DPU brought by higher-for-longer interest rates will still be apparent. We expect FY24e earnings will be supported by strong rental reversion.

The Positives

+ Resilient rental reversion of 15.7%, with 313@somerset contributing c.20%, and Jem delivering stable support of c.10%. Due to the lingering effects of COVID-19 base rents, we expect a rental reversion in the high teens for 313@somerset and in the low teens for Jem in 2025, as 20.3% of the lease by GRI is set to expire.

+ Stable operating metrics. Tenant sales continue to trend above pre-COVID levels and increased 0.6% YoY in 1H24. F&B, entertainment, and necessities outperformed. Despite lower contributions from GTO, we expect sales to benefit the top line with the influx of Chinese tourists, facilitated by the 30-day visa-free policy.

The Negative

– Borrowing cost inched up. There was no indication of a near-term reversal in the interest rate trajectory. LREIT having hedged 61% of its borrowings, will not experience much benefit from a potential interest rate cut in the future. With the implementation of the new rate, the expected interest rate for FY24e is c.3.5% (1H24: 3.37%).

Source: Phillip Capital Research - 5 Feb 2024

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Singapore Telecommunications Ltd – Down Under Is Turning Around

Created by traderhub8 | May 27, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Apps

Top Articles

1

SGX Market Dialogues

10 in 10 With NetLink NBN Trust - The Fibre of a Smart Nation

2

SGX Market Updates

4

CEO Morning Brief

Singapore Airlines’ CEO Gets Pay Jump After Record Annual Profit

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....