Trader Hub

Sheng Siong Group Ltd – Same-store Sales Inching Up

traderhub8

Publish date: Mon, 30 Oct 2023, 11:42 AM

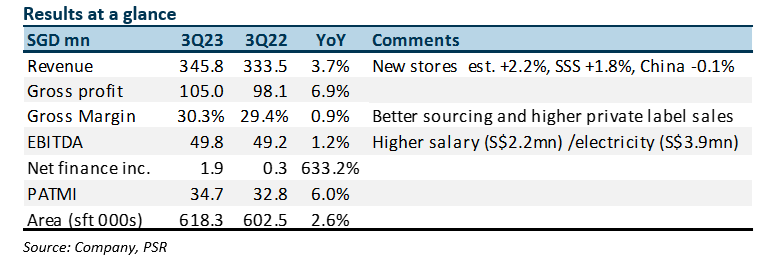

- 3Q23 results were within expectations. 9M23 revenue and PATMI were 75%/74% of our FY23e forecast. Despite, the spike in salaries and electricity cost, PATMI grew 6% YoY on improving gross margins and interest income.

- Same-store sales in 3Q23 grew 1.8% YoY, inching up from 2Q23 by 1.5%. We believe the improvement is from market share gains. Visible promotions in the community and a reputation as a cost leader helped push revenue growth.

- We expect higher earnings growth in FY24e from new stores, lower utility costs, increase in same-store sales and interest income. Our FY23e earnings and BUY recommendation is maintained. However, we are lowering our target price to S$1.80 (prev. S$1.98). Historical valuations have been creeping downward from 22x PE to 20x PE. Post- pandemic there has been a de-rating of growth expectations.

The Positives

+ Same-store sales building momentum. We have seen same-store sales turning since 2Q23. Momentum has crept up to 1.8% YoY in 3Q23, from an estimated 1.5% YoY in 2Q23. Same-store sales is rising from market share gains and a jump in population in Singapore.

+New stores recovering. SSG added one new store in Yishun. There are three more stores pending award by HDB. Thereafter, there are another 5 stores in the pipeline by HDB over the next six months.

The Negative

– Operating expenses jumped S$6.1mn YoY. The introduction of a progressive wage model and higher utility costs drove up operating expenses by S$6.1mn (or 10% YoY). Despite higher wages, the number of staff at 3200 is similar to pre-pandemic levels. Utility cost is expected to decline in FY24e.

Source: Phillip Capital Research - 30 Oct 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Singapore Telecommunications Ltd – Down Under Is Turning Around

Created by traderhub8 | May 27, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Apps

Top Articles

1

SGX Market Dialogues

10 in 10 With NetLink NBN Trust - The Fibre of a Smart Nation

2

SGX Market Updates

3

CEO Morning Brief

Singapore Airlines’ CEO Gets Pay Jump After Record Annual Profit

4

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....