Trader Hub

Raffles Medical Group Ltd – Margins Still at Record Levels

traderhub8

Publish date: Wed, 02 Aug 2023, 11:25 AM

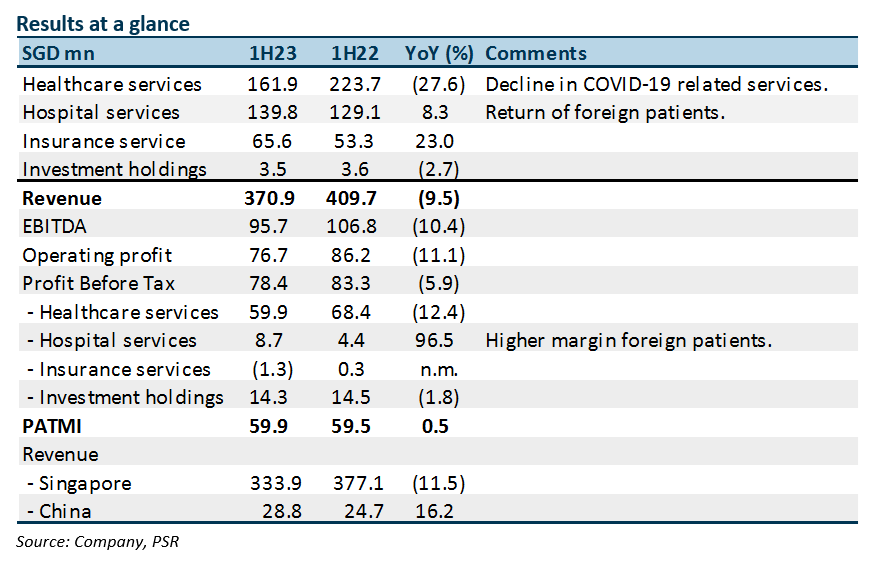

- 1H23 revenue and PATMI were within expectation at 49%/42% of our estimates. The jump in healthcare services earnings was higher than expected. PATMI was up a modest 0.5% YoY to S$59mn.

- Revenue for healthcare service was lower due to the absence of COVID-19-related services at the clinics. Hospital revenue is boosted by the return of foreign patients and transitional care facilities. Operating margins remain at record levels of around 21% despite losses in China.

- We maintain our FY23e forecast and BUY recommendation. Our DCF target price of S$1.76 is unchanged. We expect 2H23e earnings will be supported by price increases and a higher volume of foreign patients. However, the reduced contribution of COVID-19 services and lower margins from transitional care facilities (TCF) will place pressure on group margins.

The Positives

+ Resilient hospital services revenue and margins. Hospital services enjoyed growth from increased foreign patients, which are 70-80% of pre-pandemic level. Patients from Vietnam and China have not returned to pre-pandemic levels. Operating margins in 1H23 was 20.7%, higher than pre-pandemic levels of around 16%. The company managed to lower staff costs by S$34mn or 17% YoY by reducing part-time workers. Meanwhile, 1H23 PBT margin is also supported by S$4.6mn improvement in net finance income.

+ Healthy FCF* with lower capex cycle. 1H23 FCF remains strong at S$111mn (1H22: S$117mn), driving up net cash to S$230mn (1H22: S$135mn). Annualised capex is trending towards S$30mn. This compares to S$45mn p.a. over the past three years.

*Free cash flow = Operating cash-flow less Capex less Lease payments

The Negative

+ China is still a drag. Despite revenue growth of 16% YoY in 1H23, China continues to experience operating losses. The losses are estimated at between S$12mn and $14mn. The next few years are the investment phase to build brand awareness of the hospital amongst the locals. We believe locals still prefer government hospitals for their perceived pool of more experienced doctors.

Outlook

We expect 2H23 to be stable supported by the inflow of foreign patients and higher prices. Meanwhile, headwinds will stem from loss of COVID-19 PCR tests and lower margins for TCFs. Insurance will also continue suffering losses as claims rebound with the increase of more insured patients. During the pandemic, patients generally avoided the hospital if the illness was less serious.

Source: Phillip Capital Research - 2 Aug 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Singapore Telecommunications Ltd – Down Under Is Turning Around

Created by traderhub8 | May 27, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Apps

Top Articles

1

SGX Market Dialogues

10 in 10 With NetLink NBN Trust - The Fibre of a Smart Nation

2

SGX Market Updates

3

CEO Morning Brief

Singapore Airlines’ CEO Gets Pay Jump After Record Annual Profit

4

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....