Trader Hub

CapitaLand Investment Limited – Capital Recycling Picks Up Pace

traderhub8

Publish date: Mon, 29 Apr 2024, 10:21 AM

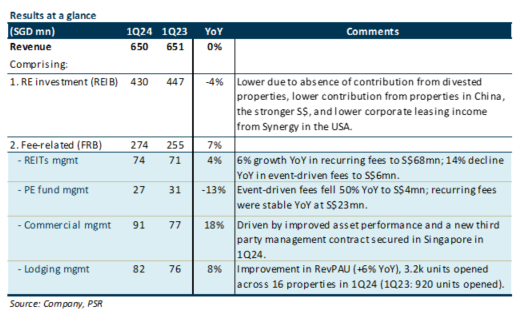

- Limited financial details were provided in this business update. 1Q24 revenue was flat YoY at S$650mn. Fee-related revenue (FRB) grew 7% YoY to S$274mn, while Real Estate Investment Business revenue (REIB) fell 4% to S$430mn.

- In 1Q24, CLI made S$600mn worth of divestments, up from S$35mn in 1Q23. More than 75% were divested into CLI’s fund vehicles. It is on track to hit its S$3bn annual divestment target, with the bulk of assets in the divestment pipeline coming from China and the USA.

- Maintain BUY with an unchanged SOTP TP of S$3.38. Our SOTP-derived TP of S$3.38 represents an upside of 32.6% and a forward P/E of 16.7x. We like CLI for its robust recurring fee income stream and asset-light model. We expect the FRB to continue to improve, supported by the lodging business as more units are opened and the return of event-driven fees.

The Positives

+ 1Q24 FRB revenue continues its growth trajectory, rising 7% YoY. This was due to improvements in commercial management fees (+18%), lodging management fees (+8%), and recurring fund management fees (+5%). Event-driven fees under the fund management platform remain a drag (-33% YoY), but we expect these to pick up this year as global transaction volumes gradually recover. Additionally, private funds recorded S$1bn in total investments in 1Q24, taking deployed funds under management to S$91bn from S$90bn in FY23. There is still S$9bn of dry powder pending deployment. CLI remains committed to double FUM to S$200bn in five years.

+ Faster pace of capital recycling. In 1Q24, CLI made S$600mn worth of divestments, up from S$35mn in 1Q23. More than 75% were divested into CLI’s fund vehicles. Divestment proceeds will be used to lower gearing and to pare down higher-cost debt. CLI is on track to hit its S$3bn annual divestment target, with the majority coming from China and the USA.

The Negative

– REIB revenue remains weak, falling 4% YoY. This was due to asset divestments, weaker operating performance in China, and lower revenue from the lodging platform Synergy in the USA.

Source: Phillip Capital Research - 29 Apr 2024

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

RHB Investment Research Reports

2

3

SGX Market Updates

STI Begins New Year With 1.8% Return, Led by Singtel & Seatrium

4

SGX Market Updates

Singapore Stocks With the Most Net Retail Buy & Sells in Early 2025

5

SGX Market Dialogues

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....