Trader Hub

Raffles Medical Group Ltd – Lacklustre Near-term

traderhub8

Publish date: Wed, 28 Feb 2024, 02:47 PM

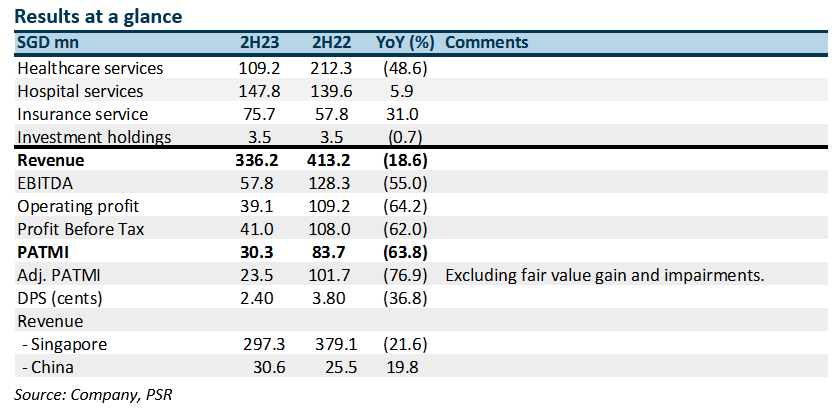

- 2023 earnings were below expectations at 89% of our estimates. 2H23 adjusted PATMI dropped 77% YoY, excluding fair value gains of S$7.4mn.

- The absence of high-margin pandemic-related services such as vaccination and testing was the major drag on earnings. Other activities pulling down margins were lower revenue per bed from transitional care facilities (TCF) and high loss ratios in their insurance business as patient claims normalised.

- We cut our FY24e PATMI by 30% to S$59.2mn. Our NEUTRAL recommendation is maintained, and the DCF target price is lowered to S$0.96 (prev. S$1.02). We do not expect any recovery in margins in the near term. Price pressure from TCF will linger due to aggressive competition. Weakness in foreign patient volume due to the strong Singapore currency, cheaper alternatives, and improved healthcare services in the region. Containing the decline in earnings will be progressive price increases in Singapore hospitals and narrowing losses in China.

The Positive

+ Growth in China. 2023 is effectively the first full year of operation for their new hospital in China, absent the pandemic interruptions. 2H23 revenue grew 20% YoY. Raffles is gradually gaining traction with foreign corporations operating in China. EBITDA break-even will require 2 to 3 years, but patient load is building momentum as marketing efforts intensify.

The Negative

– Revenue and margin collapse. Absent pandemic-related activities, including testing, vaccination, and even TCF, revenue and margins suffered. The pandemic provided extra services for Raffles and margins were high due to the urgency and limited competition.

Source: Phillip Capital Research - 28 Feb 2024

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

RHB Investment Research Reports

2

3

SGX Market Updates

STI Begins New Year With 1.8% Return, Led by Singtel & Seatrium

4

SGX Market Updates

Singapore Stocks With the Most Net Retail Buy & Sells in Early 2025

5

SGX Market Dialogues

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....