Trader Hub

Pan-United Corporation Ltd – Tailwinds From Construction Demand, Low-carbon Solutions

traderhub8

Publish date: Tue, 13 Feb 2024, 12:10 PM

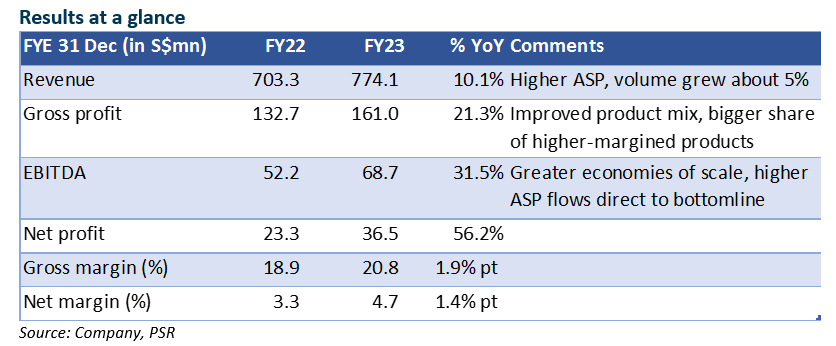

- FY23 net profit was 6% higher than our expectations. Net profit rose 56.2% YoY, lifted by higher ASP (we estimate +5%) and volume gain (+5%). Growth accelerated in 2H. 2H23 revenue gained 15% HoH, and net profit was +30%.

- Construction output in 2023 reached S$34.8bn, the highest since 2016. BCA projects output to be at S$34bn-37bn in 2024, driven by higher prices for materials and manpower. RMC volume could rise marginally to 12mn-13mn cum (average +1.6% YoY). Higher prices and higher sales of higher-margined products could sustain gross margin at 20%. The risk of customer default was reduced with about 60% of demand from public infrastructure projects, and the two integrated resorts.

- We maintain FY24e net profit estimates and a BUY recommendation. Our DCF-derived TP is raised to S$0.55 (prev. S$0.50) to reflect the strong cash flow. It increased FY23 dividend to 2.3 cents (FY22: 1.8 cents), delivering annual yield of 5.6%.

Positives

+ Achieved higher average selling price of +5% (our estimate), versus sector average of +1%., as it sold more higher-margined ready-mixed concrete products.

+ Gross margin strengthened further to 20.8% (+1.9% point YoY). We think the higher gross margin can be maintained, as low-carbon concrete products could gain wider acceptance, as a means to offset the higher carbon tax. In addition, demand for batching services, from which PanU earns a fee, is likely to be sustained. HDB has committed to launch 20,000 to 23,000 units per year through 2025.

+ ROE improved to 16.5% (FY22: 11.0%) despite net cash of S$43mn on its balance sheet. It generated FFO/share of 9.1 cents. We expect net cash to reach S$58mn at end-2024, even with higher projected capex of S$40mn to construct a new batching plant.

Negative

Nil

Source: Phillip Capital Research - 13 Feb 2024

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

THE SINGAPOREAN INVESTOR

Investing in Singapore's Hospitality Scene: A Look at the 5 Listed REITs

2

RHB Investment Research Reports

Food Empire - Expanding Ingredients Capability in Vietnam; BUY

3

RHB Investment Research Reports

ST Engineering - Rolling Forward Our Valuation; Reiterate BUY

4

CEO Morning Brief

Singapore Home Sales Set for Worst Year Since Financial Crisis

5

SGX Market Dialogues

Kopi-C With GuocoLand’s Group CEO: ‘We Have Twin Engines for Growth’

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....