Trader Hub

BRC Asia – Margins Gained From Higher Volume

traderhub8

Publish date: Tue, 13 Feb 2024, 12:10 PM

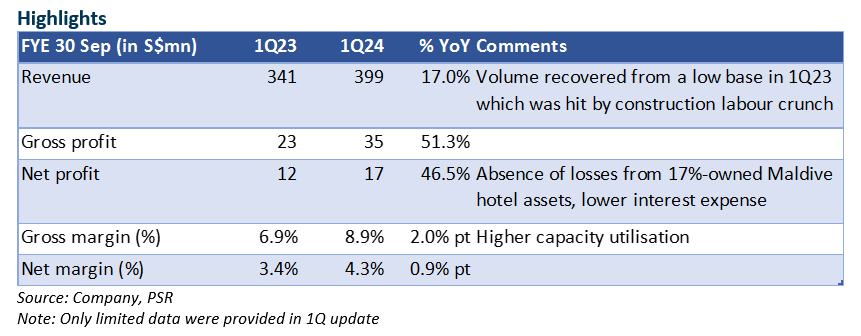

- 1Q24 net profit came in at 20% of our FY24e estimates. This is typically the lull quarter for construction output. Revenue jumped 17% YoY due to low volume in the year earlier, as the labor crunch affected activities and order deliveries. We estimate higher volume was partly offset by a 17% lower ASP for steel rebars. Net profit gained from the absence of associate losses, and lower interest expense as net gearing improved to 0.46x (Dec 22: 0.65x).

- We maintain our net profit estimates for FY24e, though there is a possible upside from a S$14mn divestment gain of the Maldives hotel assets. We estimate that the sale could also lift dividends by about S$0.05/share, which have not been factored into our numbers.

- Downgrade to ACCUMULATE (prev. BUY) due to the recent share price gain. Our TP remains unchanged at $1.99. BRC’s strong ROE of 18.6% in FY24e reflects market leadership that enables it to enjoy economies of scale. The tailwinds for FY24e are stronger construction output and the bottoming of steel prices.

The Positives

+ 1Q24 net profit surged by 46.5% YoY, on the back of volume recovery from a low base in the year earlier, the absence of losses from the 17%-owned Maldives hotel assets, and lower interest expenses. We estimate that steel prices were about 17% lower YoY.

+ Gross margin was 2.0% points higher YoY, which reflects a higher utilisation rate at its fabrication plant and possibly lower freight costs.

+ Net debt at end-Dec 23 of S$207mn was flat versus S$196mn at end-Sep 23, despite the jump in sales, suggesting still healthy working capital and no collection stress. Lower steel prices also free up trade financing needs. Net gearing as at end-Dec was 0.46x.

The Negative

– nil

Source: Phillip Capital Research - 13 Feb 2024

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

RHB Investment Research Reports

2

CEO Morning Brief

Singapore Banks Back Police Controls on Accounts to Avert Scams

3

RHB Investment Research Reports

4

5

STE's Stocks Investing Journey

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....