Trader Hub

Suntec REIT – Deeply Discounted Assets

traderhub8

Publish date: Thu, 25 Jan 2024, 10:43 AM

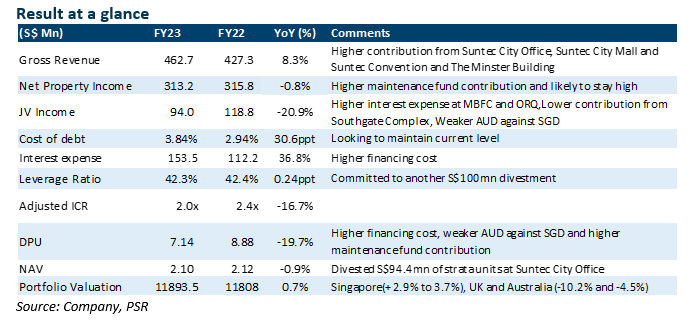

- Gross revenue for FY23 surged by 8.3% to S$462.7mn, surpassing our expectations by 7.8%. NPI slided 0.8% YoY to S$2mn and was in line with expectation at 104.2% of our forecast.Revenue were supported by a rental reversion of 12.3% for Singapore office spaces and a 21.8% rental reversion for Suntec City Mall. Suntec Convention has fully resumed its operations, with revenue surpassing pre-COVID levels by 3.9%.

- DPU decreased by 19.7% YoY but exceeded our estimates(S$307.9mn) by 6.7%, primarily due to higher maintenance fund contribution and weaker Australia performance, ending the full year at 7.135 cents. Another S$100mn divestment plan has been set, following the S$94.4mn of strata offices sold in FY23.

- We reiterate our BUY recommendation with an unchanged DDM-TP of S$1.47 and FY24e-25e DPU forecasts of S$7.30 to S$7.89 cents. We have factored in the effects of leasing downtime and a better-than-expected recovery of the Suntec Convention Center in FY24e. Rental reversions for retail spaces will continue to trend strong in the mid-teens, while office spaces are expected to be in the mid-single digits. The stock is trading at 42% discount to book value of S$2.1.

The Positives

+ Resilient balance sheet upon completion of divestment goal. SUN divested S$94.4mn at Suntec City Office Towers in FY23 at,31% above the book value. Post-divestment, gearing stood at 42.3% (-0.24ppt YoY). SUN is committed to another S$100mn disposal plan, with a priority on strata units in Suntec Office due to better visibility of end-user demand. The proceeds generated will be used for debt repayment, aiming to lower gearing to 40%. The S$200mn strata units contribute to c.5% of the total revenue, thus compressing DPU by 3% after factoring in interest savings from debt repayment.

+ Singapore valuation rose. Tenant sales surpassed the pre-COVID level by 14%, while shopper traffic lagged behind by c.10%. Singapore retail achieved a rental reversion of 21.8% in FY23 despite cautious domestic consumption. Meanwhile, rental reversion for offices remains resilient at 12.3%, with high tenant retention of 71% in Suntec. Occupancy costs continue to trend down to 21%, compared to the pre-COVID level of 23%, leaving room for further rental reversion. Singapore assets valuation rose by 3.1% in FY23. The overseas portfolio fell due to cap rate expansion, ranging from 25 bps to 63 bps, resulting in a total portfolio valuation uplift of 0.7%.

+ Better-than-expected recovery for Suntec Converntion Center. While MBS expansion faced some delays, Suntec Convention rebounded strongly in 2023 with the return of larger international events, driving revenue to grow 58%YoY to S$63.9 (+3.9% FY19). The growth is set to continue in FY24, driven by MICE and consumer events. We expect them to contribute to c.20% of total revenue.

The Negative

– Fading recovery tailwind. The retail occupancy rate saw a 2.3% YoY decline to 95.2%, mainly due to the departure of anchor tenants in both Singapore and overseas assets. The occupancy rate for 55 Currie Street was at 56.2% and is expected to improve by 1Q24. Minster Building occupancy stood at 87.3%. Portfolio occupancy for Offices segment also dropped by 3.4% YoY to 94.9%.

Source: Phillip Capital Research - 25 Jan 2024

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

2

3

Johor house best buy

4

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....