Trader Hub

BRC Asia – Construction Progress to Gather Speed

traderhub8

Publish date: Wed, 06 Dec 2023, 11:13 AM

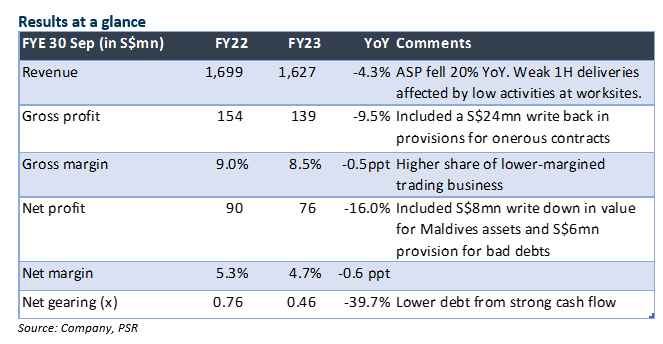

- FY23 net profit was 14.8% above our expectations due to S$24mn write-back in provisions for onerous contracts, offset by S$8mn write-down in value of its Maldives hospitality asset and S$6mn provisions for impairment/fair value loss on trade receivables.

- Net profit declined 16.0% YoY, due to 20% YoY fall in ASP (our estimate) and lower volume in 1H23 as customers faced safety measures and manpower constraints. 2H23 net profit was flat YoY. Demand remains strong, led by public sector jobs.

- Maintain BUY with unchanged TP of $1.99. We think the ASP has bottomed and will remain stable. We estimate volume could rise by 20% in FY24e as the construction sector plays catch up. We raise FY24e net profit forecast by 5.6% on less funding cost on improved gearing.

The Positives

+ Revenue and net profit rebounded in 2H23, after a weak 1H when sales of steel products were curtailed by safety rules imposed at construction sites. 2H23 revenue and net profit were flat YoY, despite the ASP decline of 27% YoY (our estimate), implying strong volume recovery.

+ Gross margin was lower (-0.5% pt to 8.5%) due to higher share of lower-margined trading business (25% of revenue). We expect it to recover to 9% in FY24e when fabrication and manufacturing volume rises. Demand for steel products remains strong. BRC’s orderbook of S$1.3bn is underpinned by mainly public sector projects.

+ Net gearing improved to 0.5x (Sep 22: 0.8x) from strong operating cash flow. EBITDA to interest expense improved to 1.5x (FY22: 2.3x).

The Negative

– nil

Outlook

Net profit growth is expected to resume with a stable ASP and stronger order deliveries. Construction demand is expected to remain robust, led by public housing, record government land sale programmes and infrastructure projects.

Maintain BUY with unchanged TP of $1.99

BRC trades at an attractive 8.9% dividend yield and 1x P/B for FY24e.

Source: Phillip Capital Research - 6 Dec 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

2

3

Johor house best buy

4

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....