Trader Hub

Prime US REIT – Challenges Remain, But Manageable

traderhub8

Publish date: Thu, 09 Nov 2023, 11:37 AM

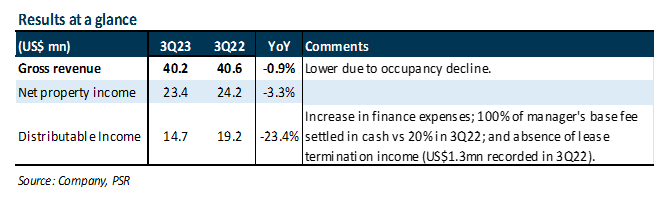

- 3Q23 distributable income of US$14.7mn (-23.4% YoY) was in line with our expectations and formed 25% of our FY23e forecast. The YoY decline was due to Prime increasing management fees paid in cash from 20% to 100%, higher interest expense, lower portfolio occupancy, and absence of lease termination income (US$1.3mn recorded in 3Q22). Excluding the change in management fees paid in cash, distributable income is down 16.6% YoY.

- Portfolio occupancy dropped to 85% from 85.6% in 2Q23, with overall rental reversions of -2%. Prime is prioritising net effective rents (deals with lower capex) over headline rents in this challenging US office environment in a bid to shore up occupancy.

- Maintain BUY, DDM-TP lowered from US$0.39 to US$0.37. FY24e DPU lowered by 7% on lower occupancy and higher finance costs assumptions. Prime is currently trading at 0.21x P/NAV. We believe that most of the negatives are already priced in. The key risk will be on the year-end valuation impact to gearing (43.7%) and bank covenants. There is a refinancing of US$484mn (69% of total) debt under its main credit facility which expires in July 24. The current share price implies FY23e/FY24e DPU yield of 30%.

The Positive

+ Leasing activities picked up in 3Q23. Prime signed 145.6k sq ft of leases in 3Q23, more than the previous two quarters combined (1H23: 131.2k sq ft). This was mainly due to the lease extension of top tenant Charter Communications for 94k sq ft at Village Center Station I (VCS I). Management indicated strong leasing momentum at some of its properties, with notable leasing discussions underway at VCS I and Park Tower, albeit with relatively longer lead times. One of its top 10 tenants, Matheson Tri-Gas, has indicated interest to expand its space at Tower 909, and discussions are ongoing.

The Negatives

– Portfolio occupancy dipped from 85.6% to 85% QoQ. We expect further decline in occupancy going forward as Sodexo, Prime’s second largest tenant (5.3% of income), vacates One Washingtonian Center (OWC). It will vacate 166k sq ft of 191k sq ft leased by Dec 2023 – the balance space is currently sublet to other tenants who will likely remain. Prime is making use of this downtime to re-amenitize OWC, with enhancement initiatives costing c.US$5mn underway to modernize the asset to improve leasing interests. Backfilling at this asset is in progress, with encouraging signs as it has already secured a 19k sq ft 11-year lease with a healthcare tenant in Oct 23.

– Gearing increased 0.9ppts QoQ to 43.7%, leaving a c.12.9% buffer from FY22 year-end valuations before it reaches 50%. 78% of debt is either on fixed rate or hedged (2Q23: 80%), with 62% of debt hedged or fixed through to 2026 or beyond. The remaining 16% of hedges expire in July 24. Prime’s YTD all in interest cost rose to 4% from 3.9% in 1H23, and its interest coverage ratio is at 3.2x. Prime is in talks with lenders to refinance US$484mn (69% of total) debt that expires in July 24.

Source: Phillip Capital Research - 9 Nov 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

2

3

Johor house best buy

4

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....