Trader Hub

Suntec REIT – the Discounted Gem

traderhub8

Publish date: Mon, 11 Sep 2023, 11:38 AM

- 1H23 revenue rose 10.2% YoY driven by strong rental reversion of Singapore assets (+17.5% yoy for Suntec City Mall, +10.8% yoy for office portfolio). Revenue for Suntec Convection surged 95.2% YoY and is expected to be back to pre-COVID level in FY24e.

- SUN is actively deleveraging with a target gearing ratio of 40% (1H23 gearing: 6%). c.S$14m divestment of strata units in Suntec Office were completed in the 1H23. SUN remains committed of the divestment and eyeing other assets such as 477 Collins Street.

- At 0.57x P/NAV (FY23e, NAV:2.13), SUN is currently trading at 0.33 SD below its mean of 0.78 P/NAV and below the average SREIT historical valuation of 0.86x P/NAV. We initiate coverage with a BUY recommendation on Suntec REIT and a DDM-based target price of S$1.47 and an annual dividend yield of 5.64% under the current share price.

Company Background

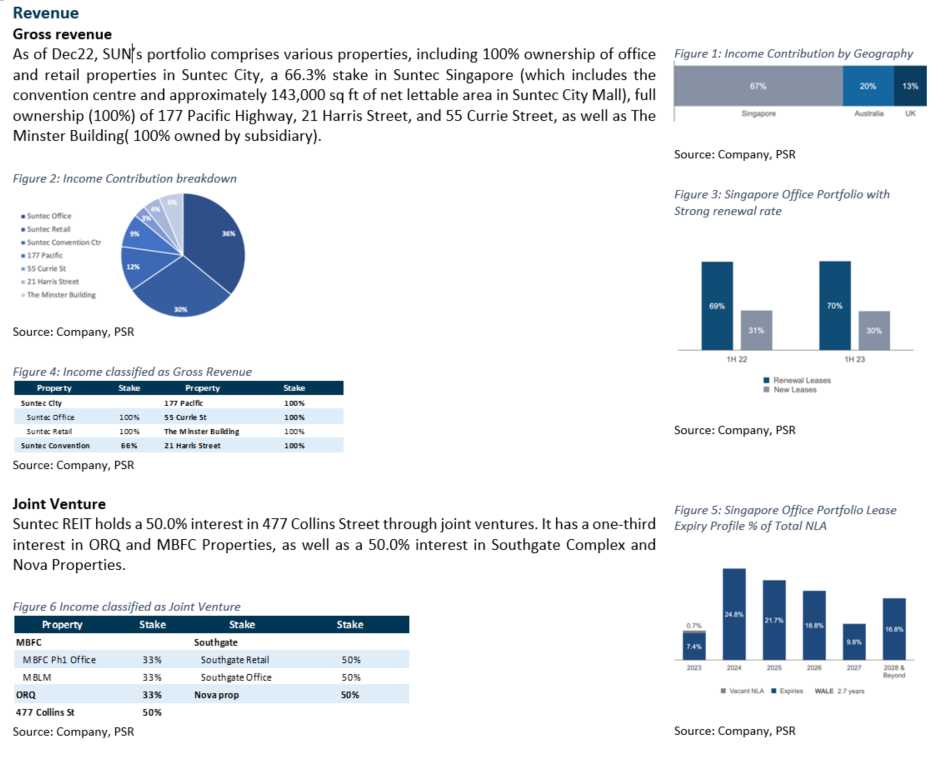

Suntec REIT (SUN) is a commercial real estate investment trust (REIT) with office and retail assets. It owns several Grade-A office buildings such as Suntec Office, a one-third stake in One Raffles Quay and a one-third stake in MBFC Towers 1 and 2. With 66.3% interest in Suntec Singapore Convention & Exhibition Centre and full ownership of Suntec City Mall, SUN owns an integrated commercial development known as Suntec City. ARA Trust Management (Suntec) Limited is the appointed manager. SUN has a diversified portfolio across geographies with 69% of revenue contributed from Singapore, 20% Australia and 13% UK.

Key Investment Merits

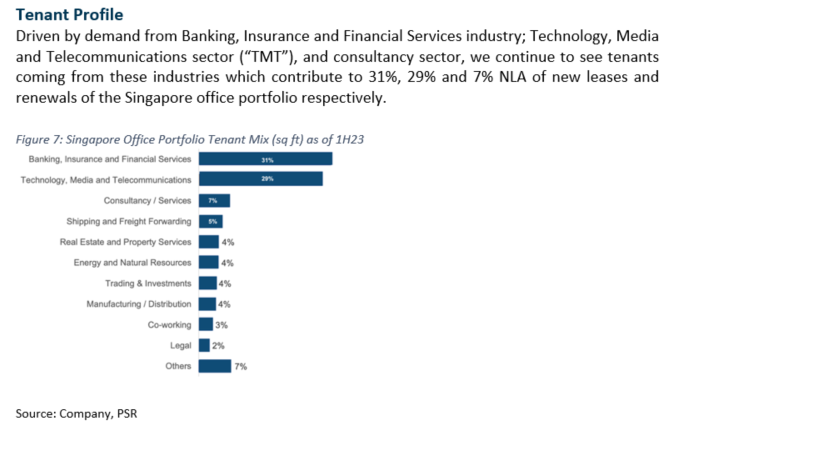

- Healthy operating metrics. In 1H23, the Singapore Offices achieved a rental reversion of 10.8% and an overall occupancy rate of 99.3%. Occupancy for Suntec City Mall remained stable at 98.3%, while rental reversion experienced a noticeable increase of +18.2% (a 1.7% QoQ growth). Tenant sales reached 108% of the pre-COVID level, with expectations of further enhancement upon the complete recovery of international tourism. Furthermore, revenue for Suntec Convention surged 95.2% YoY to 83.7% of the pre-pandemic level and the management is confident that the revenue will gradually recover back to pre-COVID level in FY24 (1H19: S$28.9m).

- Divestment over equity fundraising to lower its gearing. In 1H23, SUN successfully sold 3 strata units in Suntec Office, summing up to around 10k sqft with at least 20% above book value. Proceeds from the sales was c.S$14m. SUN is also eyeing potential divestment for mature assets such as 477 Collins Street in Melbourne (currently valued at S$433.3m). With the target of lowering the gearing to 40% (currently is at 42.6%, +20bp YoY), we believe SUN needs to divest c.S$200m worth of assets more.

- Valuation near record low. SUN is currently trading at 0.33 SD below the mean and 0.57x P/NAV (FY23e, NAV:2.13) which is below the average SREIT (0.86x P/NAV). Despite the hike in Singapore 10-year bond yield to 3.22%, SUN is still trading at a positive spread of 2.33% (FY23e). SUN can benefit the most from interest rate due to its lower fixed rate debt of 58% vs peers’ 76% (KREIT), 78.3% (MPACT) and 78% (CICT).

We initiate coverage with a BUY rating and a target price of S$1.47 based on DDM valuation, COE of 10.4% and terminal growth of 1%. We expect DPU of 6.83 cents for FY23e and 7.29 cents for FY24e, translating into yields of 5.64% and 6.03%, respectively. FY23e NPI yield is c.4.2%

Source: Phillip Capital Research - 11 Sep 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

2

3

Johor house best buy

4

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....