Trader Hub

Singapore Telecommunications Ltd – Pulled Down Under

traderhub8

Publish date: Mon, 29 May 2023, 06:10 PM

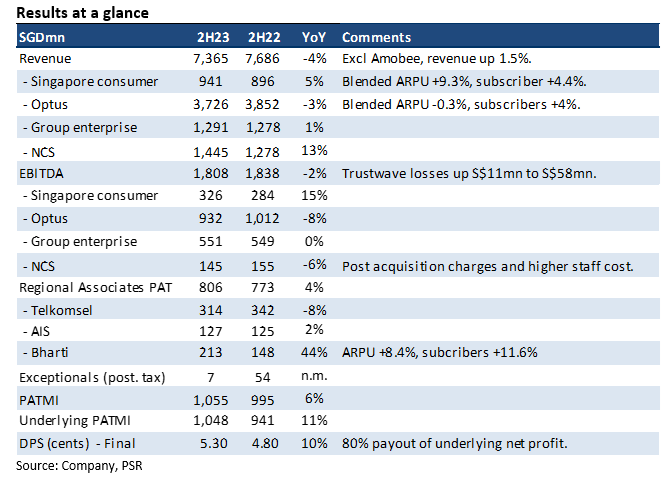

- FY23 revenue met our expectations at 103% of FY23e estimates. EBITDA was 96% of estimates. Australian dollar weakness of 7.4% YoY in 2H23 was a major drag to earnings.

- 2H23 underlying PATMI grew 11% to S$1.05bn. Almost all the growth came from lower depreciation and amortisation of S$90mn. Optus remains the major drag in earnings with its paltry ROIC of ~2% and 2H23 net profit of only A$7mn.

- We left our FY24e revenue and EBITDA relatively unchanged. Our SOTP TP of S$2.84 and ACCUMULATE recommendation is maintained. Capital management remains the largest upside with planned capital recycling of S$6bn, including disposal of Trustwave, redevelopment of Comcentre and partial monetisation of infrastructure assets (datacentre, satellite, submarine cable). Any longer-term re-rating and improvement in ROIC will include a more significant return to profitability for Optus.

The Positives

+ Re-opening boost for Singapore mobile. Mobile service revenue increased 13% YoY to S$431mn from higher ARPU (+9%) and subscribers (4%). Increased travel boosted the lucrative roaming revenue. There is further room to recover as current roaming is 60% of pre-pandemic levels. Another initiative to boost ARPU is to remove the lowest-tier pricing plans.

+ Continued strength in Bharti earnings. Earnings contribution from Bharti rose 44% YoY to S$213mn. Earnings benefited from higher ARPU (+8% YoY), increased data usage and strong 4G subscribers (+12%). However, the pace of growth should stabilise as ARPU is flat QoQ at Rp193.

The Negative

– Challenging profitability at Optus. Excluding the one-off NBN migration revenue, 2H23 EBITDA is up 1.6% YoY to A$1bn. Bulk of the revenue growth in 2H23 was from low margin equipment sales that rose 16% to A$839mn. We believe Optus is struggling to achieve any economies of scale. Indirect (non-revenue related) cost is rising in line with service revenues. The A$4.5bn of capex over the past three years has so far not generated much additional growth in revenue, in our opinion*. Meanwhile, depreciation and interest expenses are stubbornly high despite the de-gearing exercise from the sale and leaseback of its passive infrastructures completed in FY22.

Source: Phillip Capital Research - 29 May 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

2

3

Johor house best buy

4

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....