Trader Hub

CapitaLand Investment Limited – Lodging Business to Drive Growth

traderhub8

Publish date: Mon, 15 May 2023, 09:57 AM

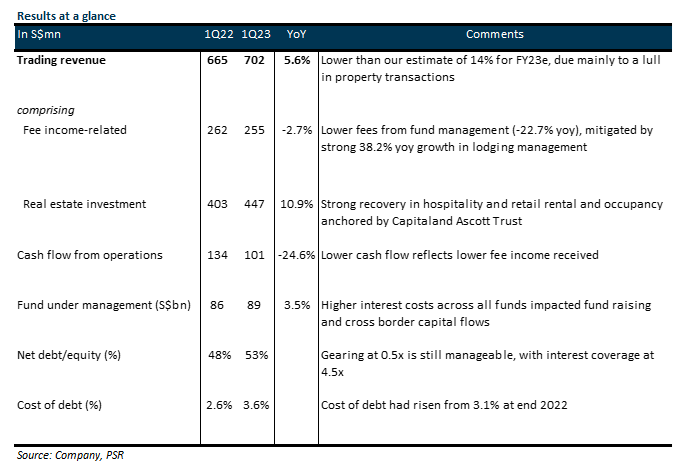

- 1Q23 revenue of S$702mn (+5.6% YoY) was slightly below our estimates, forming 21% of our FY23e forecast. This was due to lower event-driven fees from fund management (-S$33m or -68.8% YoY) with the lull in property transaction activities. Recurring fee income from fund management grew 3.5% to S$87mn.

- Revenue from the real estate investment business, which rose by 10.9% YoY, benefitted from strong recovery in the hospitality and retail sectors. CapitaLand Ascott Trust and CLI’s lodging management fees gained from higher rental and occupancy rates. 1Q23 portfolio RevPAU grew 42% YoY to reach 103% of 1Q19 pre-COVID RevPAU at S$81.

- Maintain ACCUMULATE with an unchanged SOTP TP of S$4.12. No change in estimates. Our SOTP derived TP of S$4.12 represents an upside of 17.1% and a forward P/E of 17x. The pick-up in travel and China’s continued re-opening will be immediate catalysts for CLI.

The Positives

+ Strong recovery in the lodging segment. Lodging management fee-related income grew 38.2% to S$76mn due to higher room rates as well as improved occupancy across the portfolio. Portfolio RevPAU grew 42% YoY to S$81 and is 103% of 1Q19 pre-COVID levels. The real estate investment business also benefitted from the recovery in the lodging segment, with revenue growing 10.9% YoY to S$447mn. With the FY23 target of 160k lodging units in the portfolio hit in 1Q23 after signing >4k units in 1Q23, the new target is to double its fee revenue from lodging management to >S$500mn in 5 years.

The Negatives

– 1Q23 revenue growth of 5.6% was below our estimate of 14% for FY23e, due to lower event-driven fees from fund management (-S$33m or -68.8% YoY) with the lull in property transaction activities. However, recurring fees held stable for private funds at S$23mn, while fees from listed funds grew 4.9% to S$64mn. As a result, fee related earnings from fund management fell 22.7% to S$102mn.

– Cash flow from operations fell 24.6% to S$101m, or FFO/share of 2cts. As a result, net debt/equity has risen to 0.53x, and interest coverage is lower at 4.5x. The cost of debt saw an increase of 50bp to 3.6% from end 2022, as only 62% of its debt is on fixed rate.

Source: Phillip Capital Research - 15 May 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

2

3

Johor house best buy

4

CEO Morning Brief

5

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....