Trader Hub

Lendlease Global Commercial REIT – Organic and Inorganic Growth Opportunities

traderhub8

Publish date: Mon, 24 Apr 2023, 06:05 PM

- Organic growth of an additional 10,200 sft NLA, retail footfall to benefit from upcoming tenant Live Nation, c.3% annual rental escalation from 313@somerset and c.5.7% rental escalation tied to CPI growth from Milan commercial property.

- Inorganic growth opportunities from the sponsor’s stabilised asset pipeline, of up to c.$5bn.

- Resume coverage with a BUY recommendation and DDM TP (cost of equity 7.6%) of S$0.91. Valuations are attractive at FY23e yields of 6.6%.

Key Investment Merits

Organic growth to support valuation and DPU:

- Lendlease Global Commercial REIT (LREIT) is expecting its new tenant Live Nation to be fully renovated at the end of 2024. With a capacity of more than 2,000 concertgoers per event, four events per day translate to generate additional footfall of 1mn per year which is 2.5% of the total 313@somerset footfall. We expect more than 90% of the tenants (except money changers, gadget stores, etc) to benefit from the concerts.

- LREIT is also gradually deploying its additional plot ratio of 10,200 sft, 3.4% of the total NLA of 313@somerset. If LREIT is to deploy the entire 10,200 sft, we believe the plan is to convert Level 7/ Level 6 (currently a car park) into retail and expand higher-yielding floors such as Level 1. With the additional plot ratio and the presence of Live Nation, we expect the NPI of 313@somerset to increase by 2%.

- We expect an annual rental escalation in Sky Complex Milan of 5.7% based on 75% of March 2023 CPI growth.

Potential Inorganic growth opportunities: After capping gearing at 45%, LREIT is estimated to have a debt headroom of c.$207m which allows for piecemeal acquisitions of a small stake in PLQ Mall or Parkway Parade (PP) as Singapore remains its focus. We believe LREIT can acquire c.6.2% of PLQ Mall or c.14.7% of PP, assuming the cap rate for PLQ Mall and PP is c.4.5%.

Attractive Valuation: Based on the 2% terminal growth rate, we reinitiate with a BUY recommendation, and the DDM-backed target price is $0.91. We increased the COE to 7.6% to reflect the higher interest rates. We expect FY23-24e DPUs of $4.63 – 4.78 cents.

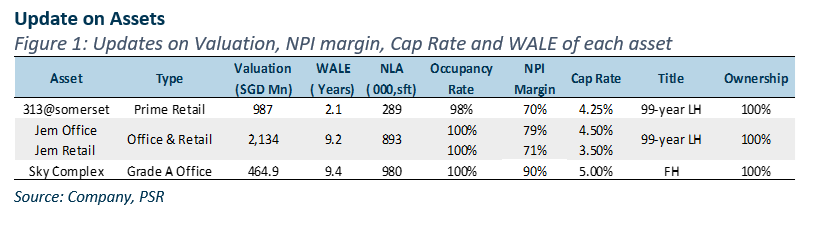

313@somerset

- 313@somerset has now positioned itself to be the incubator of new brands and businesses, a platform for business diversification from onshore to offshore. Famous brands such as TanYu and Chicha San Chen have chosen 313@somerset to initiate their pilot

- We expect a 30% decrease in CAPEX due to Live Nation taking most of the space on Grange LREIT is also actively managing its operating expenses by switching the utility contract to a lower-cost government contract.

Jem

- Office occupancy stays at 100% and it is fully leased to the Ministry of National Development.

- Tenant sales in Jem were up for c.20% YoY due to the resiliency from necessity spending and an increased footfall. We expect higher rental reversion due to the current low occupancy cost (rental charge/ tenant sales).

Sky Complex Milan

- Master tenant, Sky Italia’s lease ends in May 2032 with a physical occupancy rate at c.70% currently. The current market rental rate is c.€300-320/sqm per month, however, Sky Italia is renting at €188 / sqm. As such, we believe there is an upside in rental reversion upon lease expir

Source: Phillip Capital Research - 24 Apr 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

THE SINGAPOREAN INVESTOR

Investing in Singapore's Hospitality Scene: A Look at the 5 Listed REITs

2

RHB Investment Research Reports

Food Empire - Expanding Ingredients Capability in Vietnam; BUY

3

RHB Investment Research Reports

ST Engineering - Rolling Forward Our Valuation; Reiterate BUY

4

CEO Morning Brief

Singapore Home Sales Set for Worst Year Since Financial Crisis

5

SGX Market Dialogues

Kopi-C With GuocoLand’s Group CEO: ‘We Have Twin Engines for Growth’

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....