Trader Hub

Keppel Corporation Ltd – Asset Monetisation Drives Its Valuation

traderhub8

Publish date: Mon, 24 Apr 2023, 06:05 PM

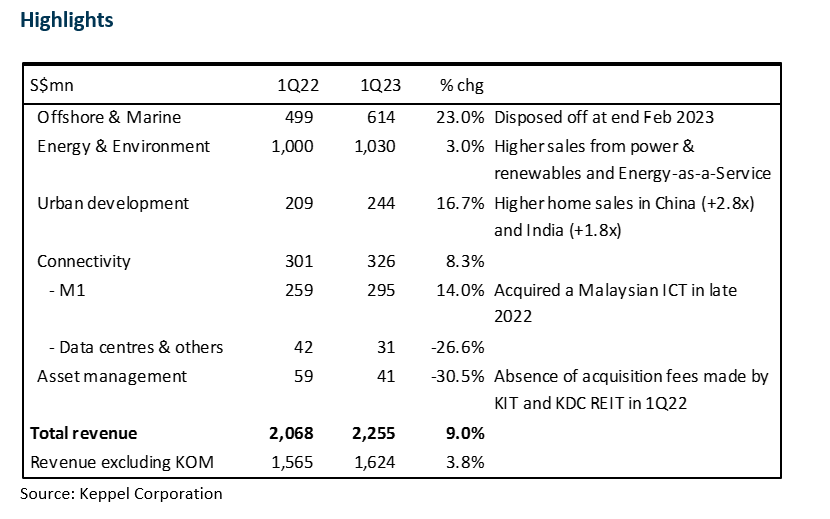

- 1Q23 revenue only rose marginally by 3% YoY, excluding the divested offshore and marine division. Urban development led the growth, driven by higher home sales in China and India. Net profit was only slightly higher.

- Disposal of Keppel Offshore & Marine resulted in a gain of S$3,300mn, but equity is reduced by S$3,845mn with the distribution-in-specie of SembCorp Marine (SMM) shares. Out-of-scope assets were sold to Asset Co in exchange for vendor notes, perpetual securities and a 10% equity stake, amounting to S$2.50/Keppel share.

- Downgrade to ACCUMULATE with a lower TP of S$7.01, from S$7.21 previously. Keppel plans to announce further transformation plans in May which could include more monetization initiatives to reach its goal of S$17.5bn.

The Positives

+ Urban development led the charge with 16.7% gain in sales. Keppel Land recorded 72% higher home sales to S$740mn, underpinned by strong China (+2.8x YoY to 830 units) and India (+1.8x YoY to 800 units). It has increased focus on trading projects, which have faster turnaround and require lower working capital. About S$280mn was raised from the disposal of 3 assets in the Philippines, Myanmar and Vietnam. We believe Keppel Land remains the key earnings driver. It accounted for 44.8% of FY22 net profit.

+ Higher sales of power, renewables and energy-related services under a subscription model. Energy and environment posted 3% growth in revenue to S$1.03bn. In addition to higher sales from power and renewable energy, Energy-as-a-Service (EaaS) offering has gained traction with > S$320m subscriptions secured. The tenure, however, is not disclosed. This covers services such as energy supply, cooling services, energy optimisation and analytics and electric vehicle charging. Renewable generation capacity grew 9% since end-2022 to 2.8GW, of which 65% is operational.

+ Disposal of Keppel Offshore and Marine resulted in a gain of S$3,300mn. It has also distributed S$3,845mn worth of SembCorp Marine shares (equivalent to S$2.19/Keppel shares) to its shareholders at end Feb. About 5% of SMM shares are still held in escrow, equivalent to S$0.237/Keppel share.

The Negatives

+ Net gearing has risen to 0.83x from 0.78x at end 2022, due also to lower total equity after the distribution-in-specie.

Source: Phillip Capital Research - 24 Apr 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

THE SINGAPOREAN INVESTOR

Investing in Singapore's Hospitality Scene: A Look at the 5 Listed REITs

2

RHB Investment Research Reports

Food Empire - Expanding Ingredients Capability in Vietnam; BUY

3

RHB Investment Research Reports

ST Engineering - Rolling Forward Our Valuation; Reiterate BUY

4

CEO Morning Brief

Singapore Home Sales Set for Worst Year Since Financial Crisis

5

SGX Market Dialogues

Kopi-C With GuocoLand’s Group CEO: ‘We Have Twin Engines for Growth’

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....