Trader Hub

Keppel DC REIT – Resilient Demand Amid Tight Supply

traderhub8

Publish date: Fri, 21 Apr 2023, 06:05 PM

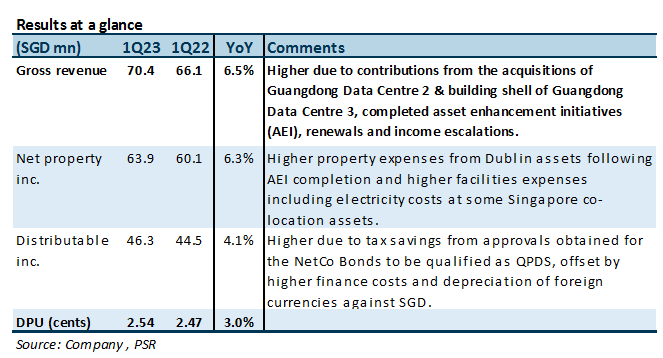

- 1Q23 DPU rose 3% YoY to 2.541 Singapore cents, due to the acquisitions of Guangdong Data Centre 2 and 3; completed asset enhancement initiatives (AEI); renewals and income escalations; and tax savings from the approval of the NetCo Bonds being qualified as Qualifying Project Debt Securities (QPDS).

- These were partially offset by lower contributions from some of its Singapore co-location assets arising from higher facilities expenses including electricity costs, higher finance costs and the depreciation of EUR, AUD and GBP against SGD.

- Downgrade from BUY to ACCUMULATE. Target price lowered from S$2.58 to S$2.26 on higher interest expense and cost of equity. Catalysts include more accretive acquisitions and lower-than-expected interest costs. The current share price implies FY23e/24e DPU yields of 4.7%/4.9%.

The Positives

+ Portfolio occupancy remained stable at 98.5% QoQ, with a portfolio WALE of 8.2 years. 14.3% of leases by rental income will expire in 2023. In our view, the likelihood of lease renewal is high due to the high costs of tenant re-location and 54% of its assets are located in Singapore.

+ Prudent capital management, with 73% of debt on fixed rate. Average cost of debt increased from 2.7% in 4Q22 to 2.8% in 1Q23. A 100bps increase in interest rates would lower DPU by c.2.2%. Gearing also edged up from 36.4% at end 2022 to 36.8%. KDCREIT has no refinancing obligations in 2023 after refinancing all loans expiring in 2023 (4.9% of total) in early April at 3-month EURIBOR plus an agreed spread. Foreign sourced income is also substantially hedged till the end of 2023, and partially thereafter until the middle of 2024. EU accounts for c.24% of income.

Outlook

Keppel DC REIT is on the lookout for acquisitions, including off-market transactions. Japan is a potential target market, where acquisition cap rates are around 5% and interest rates remain low. The sponsor also has >S$2bn worth of data centre assets under development and management that KDCREIT could potentially acquire.

There is a final payment of c.S$142mn upon the completion of Guangdong Data Centre 3, expected to take place in 3Q23. Our forecasts assume this would be funded via a cash call.

Downgrade from BUY to ACCUMULATE with a lower DDM TP of S$2.26 (prev. S$2.58)

KDCREIT’s NPI yield of 7.2% and long WALE of 8.2 years is still superior to other asset classes. Its largest tenants are some of the biggest internet enterprises in the world, with its largest contributing 35.5% of rental income. Catalysts include more accretive acquisitions and lower-than-expected interest costs. The current share price implies FY23e/24e DPU yields of 4.7%/4.9%.

Source: Phillip Capital Research - 21 Apr 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

2

3

Johor house best buy

4

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....