Trader Hub

Singapore Banking – a Quick Comparison With Credit Suisse

traderhub8

Publish date: Mon, 20 Mar 2023, 06:12 PM

- On 14 March, Credit Suisse (CS) said in its 2022 annual report that it identified “material weaknesses” in internal controls over financial reporting and had not yet stemmed customer outflows. On 15 March, the bank’s top backer, Saudi National Bank, said that it was not able to give more money to the bank due to regulatory constraints. On 16 March, the bank exercised an option to borrow up to US$54bn from the Swiss National Bank.

- Singapore banks’ capital and leverage ratios are comparable to Credit Suisse. However, Singapore banks are profitable with a positive ROE of ~12.5% (CS: -16%). Singapore banks has a larger proportion of net interest income while CS is fee and commissions.

- Maintain OVERWEIGHT. We remain positive on Singapore banks. Bank dividend yields are attractive at 5.7% with possible upside surprise due to excess capital ratios and push towards higher ROEs. Singapore banks differ from Credit Suisse as they focus on NII growth and hence are able to post positive ROEs.

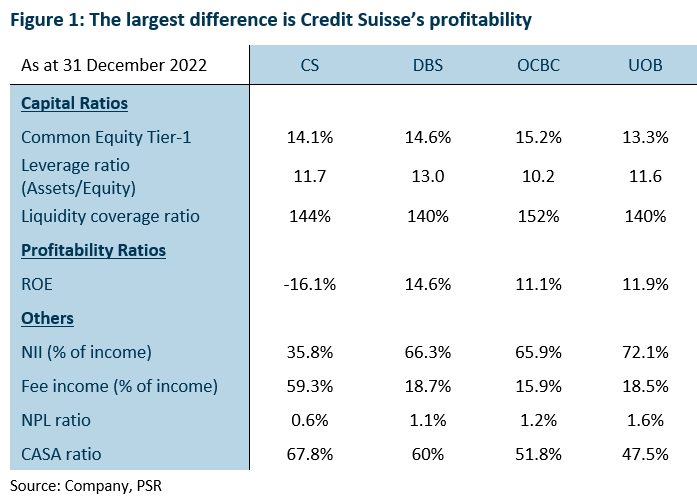

Capital and leverage ratios similar to Singapore banks

Credit Suisse’s Common Equity Tier-1 (CET1) ratio of 14.1% is comparable to Singapore banks at ~14.4%. The leverage ratio of 11.7x is similar to Singapore banks’ ~11.6x. Credit Suisse is subjected to the Liquidity Coverage Ratio (LCR) requirements by the Federal Reserve and has kept an adequate LCR of 144%, which is comparable to that of Singapore banks at ~144%. The issue with what is happening at Credit Suisse does not appear to be its capital ratios.

Two years of net losses for Credit Suisse

Credit Suisse reported two consecutive years of net losses, CHF7.29bn in FY22 and CHF1.65bn in FY21, as investment banking revenues slumped and clients pulled money from the group’s wealth management business. This resulted in a negative ROE of 16.1% for FY22.

In comparison, the Singapore banks have been posting record revenues and profits, mainly due to the higher net interest income from the higher interest rate environment. Consequently, the Singapore banks have reported an ROE of ~12.5%.

Credit Suisse’s focus is on commissions and fees

Largely an investment bank, Credit Suisse’s focus is on commissions and fee income, with fee income making up 59% of its total income and net interest income only making up 36% of total income.

For the Singapore banks, the focus is mainly on net interest income with NII making up ~68% of total income and fee income making up ~18% of total income. The local banks were able to benefit from the rise in interest rates as they were able to pass on the higher funding costs directly to their customers as the majority of the loans were on a floating rate and could be repriced.

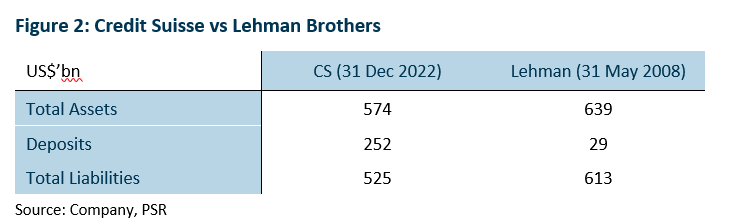

Smaller asset size compared to Lehman Brothers

Interestingly, if we were to compare Credit Suisse to Lehman Brothers back in 2008, Credit Suisse’s total assets are smaller at US$574bn compared to Lehman Brother’s total assets of US$639bn, and total liabilities are also smaller at US$525bn compared to Lehman Brother’s total liabilities of US$613bn. However, Credit Suisse has a larger amount of customer deposits, US$252bn, as compared to Lehman Brother’s customer deposits of US$29bn.

Investment Action

Maintain OVERWEIGHT. We remain positive on Singapore banks. Bank dividend yields are attractive at 5.7% with possible upside surprise due to excess capital ratios and push towards higher ROEs. Singapore banks differ from Credit Suisse as they focus on NII growth and hence are able to post positive ROEs.

Source: Phillip Capital Research - 20 Mar 2023

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

THE SINGAPOREAN INVESTOR

Investing in Singapore's Hospitality Scene: A Look at the 5 Listed REITs

2

RHB Investment Research Reports

Food Empire - Expanding Ingredients Capability in Vietnam; BUY

3

RHB Investment Research Reports

ST Engineering - Rolling Forward Our Valuation; Reiterate BUY

4

CEO Morning Brief

Singapore Home Sales Set for Worst Year Since Financial Crisis

5

SGX Market Dialogues

Kopi-C With GuocoLand’s Group CEO: ‘We Have Twin Engines for Growth’

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....