Trader Hub

Del Monte Pacific Limited – FX and Weak Festive Spend a Drag

traderhub8

Publish date: Wed, 15 Mar 2023, 06:13 PM

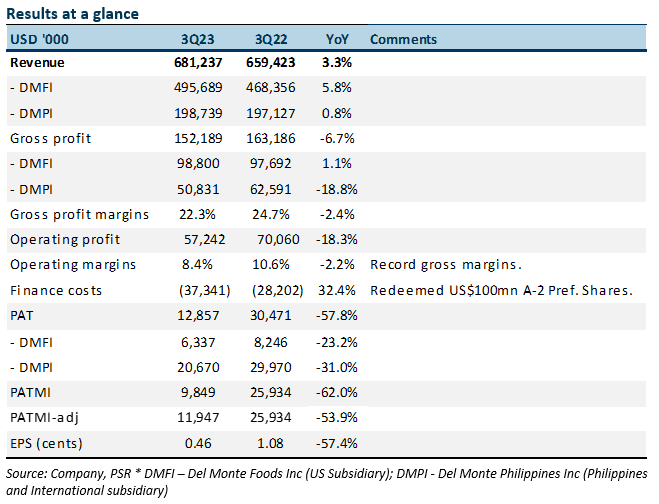

- 3Q23 earnings were below expectations. 9M23 revenue and PATMI was 73%/67% respectively of our forecast. Gross margins contracted much larger than expected.

- The weakness in earnings was due to a 12% decline in the Philippine peso and disappointing festive demand in China and the Philippines.

- We cut our F23e earnings by 18% to adjusted US$101mn. Del Monte remains a market leader in multiple consumer products in the US and the Philippines. Gross margins will remain subdued. Price increases have slowed and higher-priced inventory is hurting margins. The huge inventory post-festive period of $1bn raises the risk of write-offs. We maintain our BUY recommendation and cut our target price to S$0.40 (prev. S$0.67), pegged to 6x FY23e P/E, a 50% discount to the industry valuation due to its smaller market cap and higher gearing. Del Monte valuations remain attractive at 4x PE FY23e and an 8% dividend yield.

The Positives

+ Market shares maintained. Del Monte maintained market share in most product categories. In the US, market share in fruit cup snacks and canned fruits and vegetables was retained at 22-30%. Dominance in the Philippines was unchanged – packaged pineapple (95.7%), tomato sauce (84.6%), canned mixed fruit (74.9%) and RTD juice ex-foil pouches (45.5%).

The Negatives

– Double whammy in Asia. 3Q23 revenue at DMPI was flat YoY. The two factors driving the weakness were; 1) 12% decline in the Philippine peso: In constant currency, revenue rose 13% YoY to PHP11.3bn, but a 12% decline in peso drove down revenue growth; 2) Weak festive sales: Demand for canned tropical fruit in the Philippines and fresh pineapple sales to China were below expectations. The volume bump during the holiday season did not occur. Phillipines suffered from weak consumer demand for discretionary items. The lockdown affected sales.

– Weak gross margins in the US. 3Q23 gross margins for US operations collapsed by 8 percentage points to 20.4%. The decline was a surprise despite price increases. The reason for the weakness was the higher cost inventory of raw materials being sold. For instance, in 1H23 sales, 70-80% of the inventory was procured in FY22. Other costs remain elevated such as energy and fuel.

– Elevated inventory. Del Monte exited the festive period with a record US$1.14bn of inventory as of Jan23. The rise in value was in part due to inflationary pressure but inventory days have jumped to 204 days, compared to 149 days a year ago. We worry there is a risk of provisions with the huge jump in inventory.

Source: Phillip Capital Research - 15 Mar 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

THE SINGAPOREAN INVESTOR

Investing in Singapore's Hospitality Scene: A Look at the 5 Listed REITs

2

RHB Investment Research Reports

Food Empire - Expanding Ingredients Capability in Vietnam; BUY

3

RHB Investment Research Reports

ST Engineering - Rolling Forward Our Valuation; Reiterate BUY

4

CEO Morning Brief

Singapore Home Sales Set for Worst Year Since Financial Crisis

5

SGX Market Dialogues

Kopi-C With GuocoLand’s Group CEO: ‘We Have Twin Engines for Growth’

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....