Trader Hub

Raffles Medical Group Ltd – Policies, Immunity Debt, Tourism Helped

traderhub8

Publish date: Mon, 06 Mar 2023, 06:15 PM

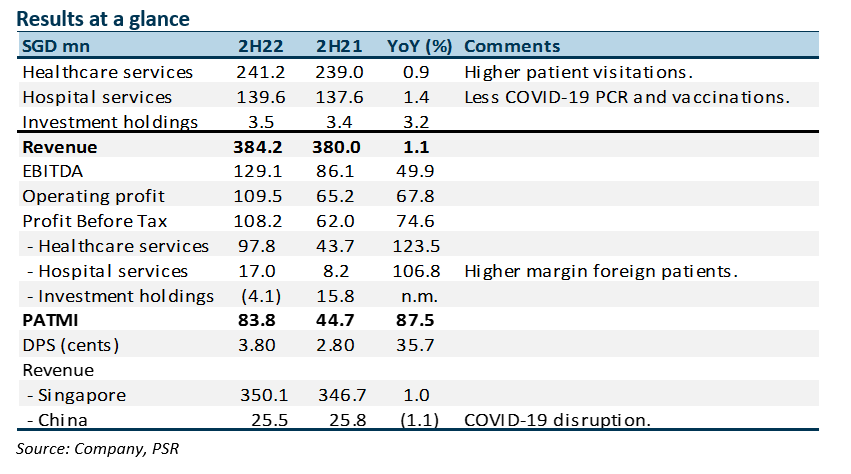

- FY22 revenue was within expectation, but PATMI was a massive beat. FY22 revenue and PATMI were 102%/143% of our estimates. The jump in healthcare services earnings was higher than expected.

- The drop in COVID-19-related revenue was offset by higher margin foreign patients, more elective surgeries, increased GP clinic visitations and additional bed capacity in Changi under the Transitional Care Facilities (TCF).

- The re-opening of borders and relaxation of social restrictions triggered the return of medical tourists. There was a wave of other infections raising the volumes at GP clinics and TCFs. We expect the TCF to be operational until public hospital capacity is meaningfully increased. Our BUY recommendation is maintained. FY23e earnings forecast is increased by 50% to S$142mn and our DCF target price raised to S$1.76 (prev. $1.46) with a higher discount rate to 8.0% (prev. 7.6%) as the risk-free rate was lifted.

The Positives

+ Spike in healthcare services earnings. 2H22 PBT for healthcare services more than doubled to S$97.8mn. The jump was due to higher GP visits as re-opening saw a jump in non-COVID infections. In addition, patients with COVID-19 symptoms preferred GP visits rather than hospitals. Increased volumes boosted operating leverage for the business.

+ Return of foreign patients. With borders re-opening, revenue from foreign patients has returned to close to pre-pandemic levels. Such patients have higher revenue intensity and better margins. We expect the return of foreign patients to continue into 1H23. We believe foreign patient revenue has surged back to around 20% of revenue. This is below the estimated 25-30% pre-pandemic.

+ Jump in FCF*. In line with the record earnings, FCF rose 51% to a record S$183mn for FY22. Capital expenditure should normalise to S$30mn-35mn after the major ramp-up of the past 3 years for the new hospitals in China. Net cash has doubled from S$90.7mn to S$180mn. FY22 dividend was increased by 36% to 3.8 cents.

*Free cash flow = Operating cash-flow less Capex less Lease payments

The Negative

+ Losses in China hospitals. EBITDA losses in China were larger than expected due to the lockdown. There was vaccination work, but revenue was low. The decline in foreigners was another negative, especially for the Beijing hospital. We expect S$10mn EBITDA loss per hospital for Chongqing and Shanghai.

Source: Phillip Capital Research - 6 Mar 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

THE SINGAPOREAN INVESTOR

Investing in Singapore's Hospitality Scene: A Look at the 5 Listed REITs

2

RHB Investment Research Reports

Food Empire - Expanding Ingredients Capability in Vietnam; BUY

3

RHB Investment Research Reports

ST Engineering - Rolling Forward Our Valuation; Reiterate BUY

4

CEO Morning Brief

Singapore Home Sales Set for Worst Year Since Financial Crisis

5

SGX Market Dialogues

Kopi-C With GuocoLand’s Group CEO: ‘We Have Twin Engines for Growth’

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....