Trader Hub

Venture Corporation Limited – Outlook Starting to Dim

traderhub8

Publish date: Mon, 27 Feb 2023, 06:18 PM

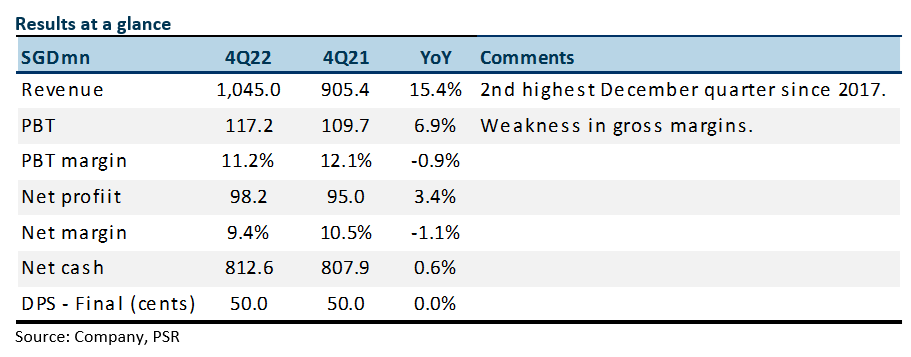

- FY22 results were within expectations. Revenue and PATMI were 102%/97% of our FY22e forecast. 4Q22 PAT rose 3.4% YoY. Gross margin was the weakest in seven years.

- There was caution in the company’s outlook. The environment in the short term is uncertain. Healthcare, life science and semiconductor sectors are the medium-term opportunities with their long product cycles.

- We lower our FY23e PATMI by 9% to S$359mn and downgrade our recommendation from BUY to ACCUMULATE. Our target price is lowered to S$19.70 (prev. S$20.80), 16x PE FY23e. The macro backdrop for electronic exports has declined significantly and the global economy slowing.

The Positive

+ Healthy growth in revenue. 4Q22 revenue grew 15% YoY to S$1.04bn, the 2nd highest December quarter since 2017. Growth was from the life science, medical device and healthcare domain. Pre-pandemic, revenue growth was a negative 4% from FY17 to FY19. We also expect revenue growth to slow in 2023 with the absence of the Malaysia re-opening lift experienced in 2022.

The Negative

– Major decline in margins. 2H22 gross margins declined 2.1% points to 23.7%, the lowest levels since 2015. We believe Venture had to absorb the higher-priced raw materials which were bulked up over the past few quarters. Venture still maintains a high S$1bn of inventories. There was operating leverage at the operating cost level due to the appreciating US dollar.

Source: Phillip Capital Research - 27 Feb 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

THE SINGAPOREAN INVESTOR

Investing in Singapore's Hospitality Scene: A Look at the 5 Listed REITs

2

RHB Investment Research Reports

Food Empire - Expanding Ingredients Capability in Vietnam; BUY

3

RHB Investment Research Reports

ST Engineering - Rolling Forward Our Valuation; Reiterate BUY

4

CEO Morning Brief

Singapore Home Sales Set for Worst Year Since Financial Crisis

5

SGX Market Dialogues

Kopi-C With GuocoLand’s Group CEO: ‘We Have Twin Engines for Growth’

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....