Trader Hub

United Overseas Bank Limited – Rise in NII Offset by Higher Allowances

traderhub8

Publish date: Mon, 27 Feb 2023, 06:17 PM

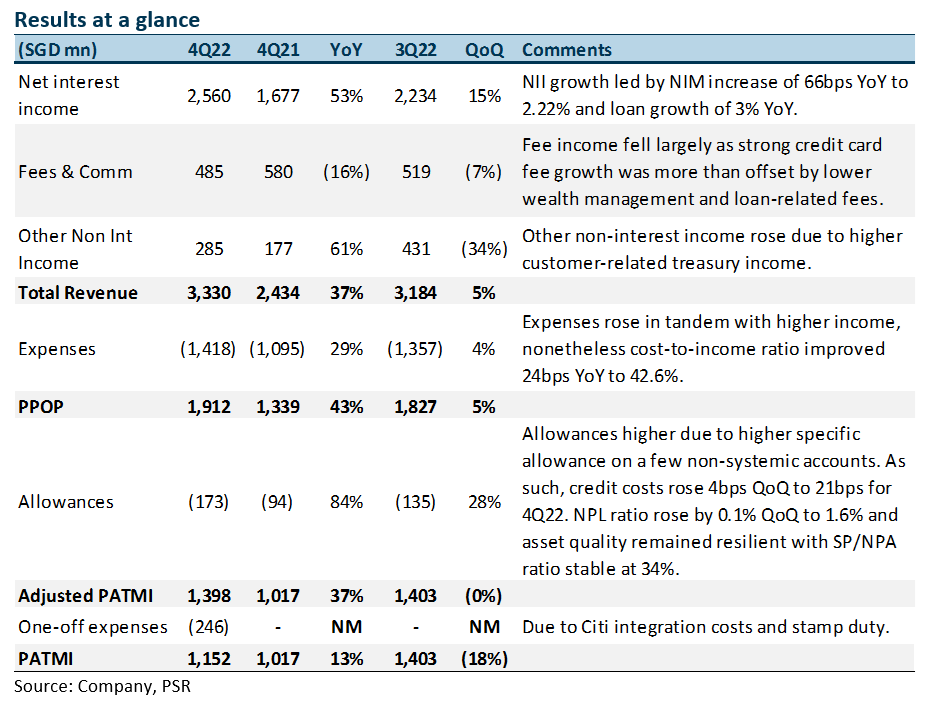

- 4Q22 adjusted earnings of S$1,398mn were slightly below our estimates due to lower fee income and higher allowances offset by NII growth. FY22 adjusted PATMI was 96% of our FY22e forecast. 4Q22 DPS was up 25% YoY to 75 cents; full-year FY22 dividend rose 13% YoY to 135 cents.

- 4Q22 NII was up 53% YoY from a NIM increase of 66bps YoY to 2.22% and loan growth of 3% YoY. Fee income fell 16% YoY due to lower WM and loan-related fees, while other non-interest income was up 61% YoY. Management is guiding mid-single digit loan growth with higher NIM of 2.2%, double-digit fee income growth, stable cost-to-income ratio and stable credit costs for FY23e.

- Maintain BUY with an unchanged target price of S$35.70. We raise FY23e earnings by 3% as we increase NII and fee income estimates for FY23e. We assume 1.48x FY23e P/BV and ROE estimate of 12.9% in our GGM valuation. Continued NIM and NII improvement and fee income recovery will boost earnings.

The Positives

+ NII spiked 53% YoY; NIM surged by 66bps. NII grew 53% YoY, despite a slowdown of loans growth to 3% YoY, while NIM surged 66bps YoY to 2.22% (QoQ: 1Q22: +2bps, 2Q22: +9bps, 3Q22: +28bps, 4Q22: +27bps). Loan growth YoY was broad-based across most territories, while the consolidation of Citi assets added 11% to the ASEAN loan book in 4Q22. UOB has maintained its guidance of mid-single digit loan growth for FY22e.

+ Other non-interest income increased by 62%. Other NII increased 62% YoY largely due to the higher customer-related treasury income which was driven by hedging demands. However, other NII fell 34% QoQ as it normalized after an exceptional 3Q22 that benefitted from market volatility.

+ New NPAs fall 42% YoY. New NPA formation fell by 42% YoY to S$395mn as asset quality stabilised during the quarter. The NPL ratio remained stable YoY at 1.6%. Asset quality remained resilient with SP/NPA stable at 34%. 4Q22 NPA coverage is at 98% and unsecured NPA coverage at 207%.

The Negatives

– Fee income continues to decline. Fees fell 16% YoY largely due to lower wealth and fund management fees as investor sentiment remained subdued alongside a seasonally softer quarter. Loan-related fees also fell 17% YoY this quarter. Nonetheless, credit card fees were higher 40% YoY mainly from higher customer spends which were boosted by the Citi consolidation.

– Credit costs increase due to higher SPs. Total allowances rose by 84% YoY to S$173mn mainly due to specific allowance increasing by 49% YoY to S$253mn on a few non-systemic accounts despite a general allowance write-back of S$80mn during the quarter (4Q21: write-back of S$76mn). This resulted in credit costs increasing by 9bps YoY to 21bps. Nonetheless, total general allowance for loans, including RLARs, was prudently maintained at 0.9% of performing loans. Full year FY22 credit cost was unchanged at 20bps and UOB has guided for credit cost of 20-25 bps for FY23e.

– Expenses up 29% YoY. Excluding one-offs, expenses rose 29% YoY to S$1,418mn in 4Q22, at the upper end of UOB’s guidance for FY22. The increase was mainly due to higher variable bonuses and pay adjustments for staff to remain more competitive and prevent the outflow of staff. IT-related expenses also increased during the quarter. Nonetheless, the cost-to-income ratio (CIR) improved 2.4% YoY to 42.6%, with full-year FY22 CIR at 43.4%. UOB has guided for a similar CIR of 43% – 44% for FY23e, and to trend below 42% by FY24e.

Source: Phillip Capital Research - 27 Feb 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

THE SINGAPOREAN INVESTOR

Investing in Singapore's Hospitality Scene: A Look at the 5 Listed REITs

2

RHB Investment Research Reports

Food Empire - Expanding Ingredients Capability in Vietnam; BUY

3

RHB Investment Research Reports

ST Engineering - Rolling Forward Our Valuation; Reiterate BUY

4

CEO Morning Brief

Singapore Home Sales Set for Worst Year Since Financial Crisis

5

SGX Market Dialogues

Kopi-C With GuocoLand’s Group CEO: ‘We Have Twin Engines for Growth’

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....