Trader Hub

ComfortDelGro Corp Ltd – Weighed by Upfront Costs

traderhub8

Publish date: Mon, 27 Feb 2023, 06:16 PM

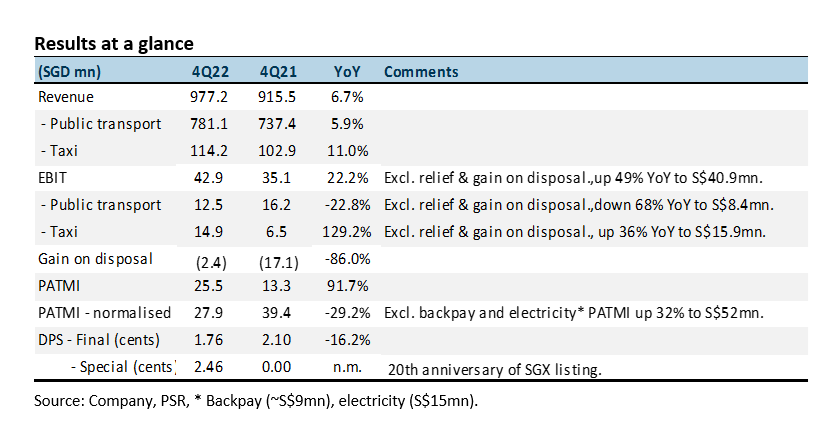

- FY22 revenue met expectations at 99% of our forecast. Adjusted PATMI was 13% below due to an additional S$15mn rail electricity expense from the new contract in Singapore. Cost recovery will come from the 13.5% fare adjustment effective late December 2022.

- Special dividend of 2.46 cents was declared to mark the 20th anniversary of the SGX listing. FY22 total special dividend was 3.87 cents while the ordinary dividend was 4.61 cents (3.8% yield).

- We lowered our FY23e PATMI by 20% to S$178.4mn as the timing of the indexation of the UK bus contract is unclear. Nevertheless, we expect earnings growth in FY23e from increased passenger volumes for both taxis and trains, re-pricing of rail fares in Singapore, indexation of UK bus contracts and reduction of taxi rebates in China. We maintain BUY with a reduced DCF target price of S$1.63 (prev. S$1.75).

The Positives

+ Taxi recovery on track. 4Q22 operating profit (excluding relief and gain on disposal) jumped 36% YoY to S$15.9mn. Earnings recovery on the back of lower rental discounts and introduction of booking commissions (May 22: 4%, Oct 22: 5%). Booking volumes in FY22 rose 31% to 34mn.

+ Piling up cash. Net cash in FY22 rose S$97mn to S$675mn. Free cashflow generated during the year was S$266mn. Gross CAPEX on vehicles was around S$300mn. FY23e CAPEX might be slightly higher for EV taxis, the PHV car rental fleet and EV charging stations. CAPEX is still below the S$400mn-500mn p.a. spent pre-pandemic.

The Negative

– China, UK and Ireland’s weak operating performance. We estimate UK and Ireland suffered a S$13mn operating loss in 4Q22 due to the one-off S$9mn UK bus driver pay deal backpay agreement. China operating earnings were down 60% to S$10.3mn in FY22 due to taxi rental rebates of S$11mn.

Source: Phillip Capital Research - 27 Feb 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

THE SINGAPOREAN INVESTOR

Investing in Singapore's Hospitality Scene: A Look at the 5 Listed REITs

2

RHB Investment Research Reports

Food Empire - Expanding Ingredients Capability in Vietnam; BUY

3

RHB Investment Research Reports

ST Engineering - Rolling Forward Our Valuation; Reiterate BUY

4

CEO Morning Brief

Singapore Home Sales Set for Worst Year Since Financial Crisis

5

SGX Market Dialogues

Kopi-C With GuocoLand’s Group CEO: ‘We Have Twin Engines for Growth’

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....