Trader Hub

Prime US REIT – Strong Rental Reversions to Drive Growth

traderhub8

Publish date: Fri, 17 Feb 2023, 06:20 PM

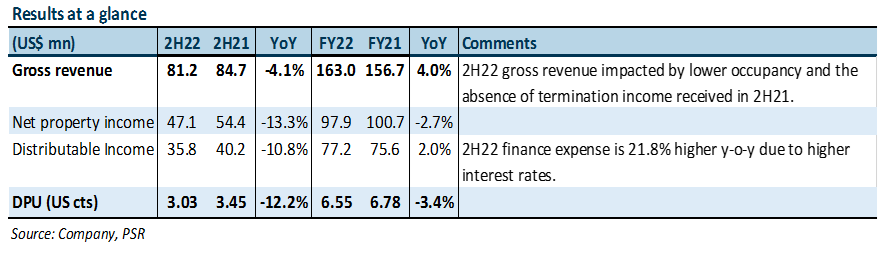

- FY22 DPU of 6.55 US cts was slightly below our estimates, mainly due to higher interest expense (+27.2%) and lower occupancies (89.1%).

- Despite portfolio valuation declining 6.7% on higher discount and cap rate assumptions, gearing at 42.1% and interest coverage at 4.1x remains well within regulatory limits.

- Maintain BUY, DDM-TP lowered from US$0.88 to US$0.70 as we lower our FY23e-FY25e DPU forecasts by 12-15% due to lower occupancy and higher financing costs. Our cost of equity increased from 10.55% to 11% as we roll forward our forecasts. PRIME is our top pick in the US office sector for greater tenant exposure to STEM/TAMI sectors. Catalysts include improved leasing and a greater return to office. Prime is currently trading at 0.6x P/NAV and below pandemic lows, and we believe that most of the negatives are already priced in. The current share price implies FY23e/FY24e DPU yield of 13.6/14.7%.

The Positives

+ Strong positive rental reversions of 20.2% for 4Q22, continuing the trend of positive rental reversions for 11 consecutive quarters. Occupancy remained relatively stable, declining 0.5% QoQ to 89.1%. Leasing remains active, with activity coming from sectors such as scientific R&D services, finance, biotechnology, manufacturing and legal services. The 20.2% reversion was substantially from Crosspoint, where an existing tenant downsized from 84k sq ft to 57.5k sq ft and extended the lease to 2032, and a new tenant backfilled space and signed a lease till 2034 at >25% reversions.

+ 82% of debt is on fixed rate or hedged, with 66% of the total debt hedged or fixed through to mid-2026 and beyond. Prime has no refinancing obligations till July 2024. Prime’s gearing increased to 42.1% from 38.7% QoQ, mainly due to the decline in portfolio valuation, but remains well within regulatory limits. Its interest coverage ratio of 4.1x is also well above MAS’ threshold of 2.5x to bring gearing limits up to 50%. Prime’s effective interest rate crept up to 3.4%, from 3.1% in 3Q22.

The Negative

– Portfolio value declined 6.7% due to higher discount and cap rate assumptions used by valuers. Across the board, cap rates increased by 50bps. All assets saw a valuation decline, with Reston Square (-14.2%, due to the non-renewal of anchor tenant), Village Center Station I (-12.1%) and One Town Center (-10.6%) having the biggest percentage declines.

Source: Phillip Capital Research - 17 Feb 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

THE SINGAPOREAN INVESTOR

Investing in Singapore's Hospitality Scene: A Look at the 5 Listed REITs

2

RHB Investment Research Reports

Food Empire - Expanding Ingredients Capability in Vietnam; BUY

3

RHB Investment Research Reports

ST Engineering - Rolling Forward Our Valuation; Reiterate BUY

4

CEO Morning Brief

Singapore Home Sales Set for Worst Year Since Financial Crisis

5

SGX Market Dialogues

Kopi-C With GuocoLand’s Group CEO: ‘We Have Twin Engines for Growth’

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....