Trader Hub

Thai Beverage PLC – a Slow Start to FY23

traderhub8

Publish date: Mon, 13 Feb 2023, 06:22 PM

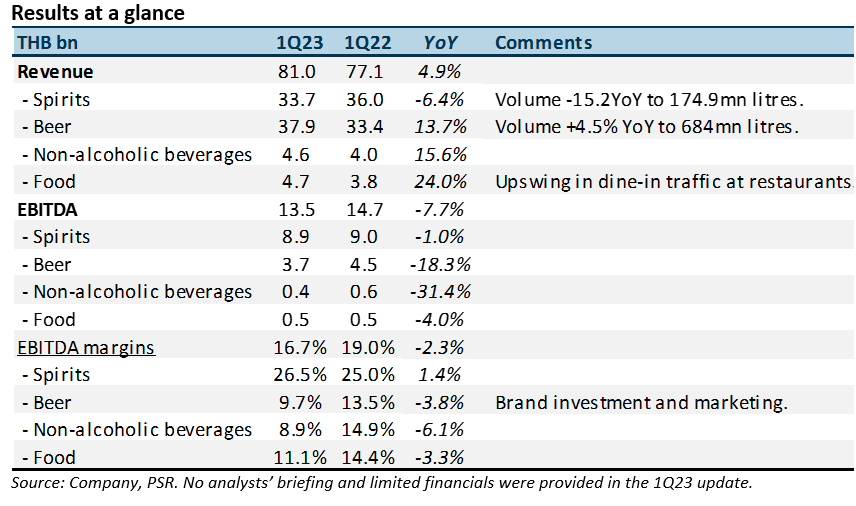

- 1Q23 revenue/EBITDA was below expectations at 27%/and 25% of our FY23e forecasts, respectively. 1Q is a seasonally stronger quarter.

- 1Q23 spirits volume contracted 15% YoY to 175mn litres after record volumes a year eariler, which enjoyed trade-inventory loading ahead of price increases.

- Our FY23e earnings are maintained. We expect earnings to recover with the re-opening of borders in Thailand, event-driven spending from the election and improvement in economic conditions. Our BUY recommendation is downgraded to ACCUMULATE following the recent share price performance. The target price of S$0.80 is unchanged at 18x FY23e core earnings, its 5-year average.

The Positive

+ Rebound in beer revenue. Beer continued to enjoy revenue growth of 13.7% YoY driven primarily by higher prices. The uptick in volumes was a more modest 4.5% YoY to 684mn litres. Sales growth in Vietnam is expected to weaken near-term due to the weakening economy, especially in manufacturing. Sabeco could pick up some volumes if consumers trade down from mass premium to mainstream brands.

The Negative

– Weak spirit volumes. Revenue declined 6.4% YoY, dragged down by a contraction of volumes by 15.4% YoY. Offsetting the weak volumes were higher prices and a better sales mix of brown spirits (vis-à-vis white spirits). A year ago volumes benefitted from front-loading of volumes ahead of price increases.

Outlook

1Q23 faced tough comparables due to the heavy front-loading of volumes a year ago. Even excluding the base effect, volumes declined 8% against 1Q21. We worry higher prices may have negatively impacted volumes. Margins are also weaker from higher marketing spend to boost brand-building after cut-backs during the pandemic.

Downgrade from BUY to ACCUMULATE with unchanged TP of S$0.80

Our target price stays at S$0.80, based on 18xFY23e earnings, its 5-year average, plus associate market cap.

Source: Phillip Capital Research - 13 Feb 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

2

3

Johor house best buy

4

CEO Morning Brief

5

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....