Trader Hub

Thai Beverage PLC – Bounce in Beer and Property

traderhub8

Publish date: Mon, 05 Dec 2022, 05:48 PM

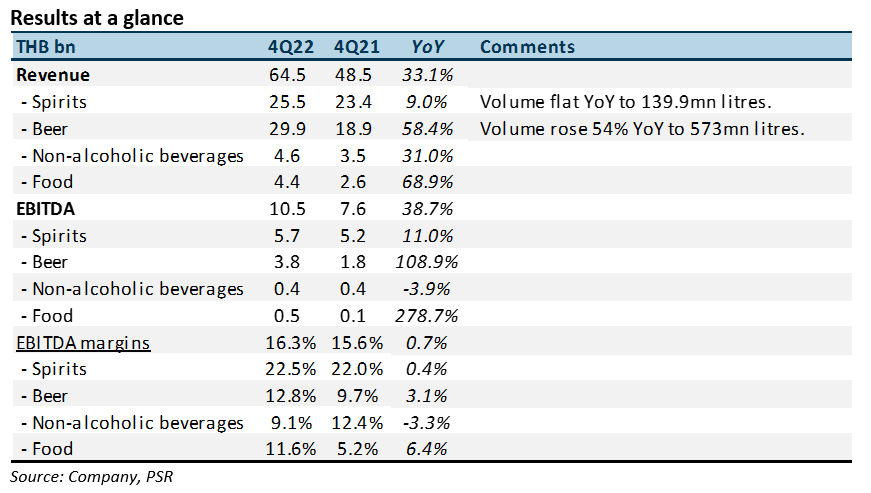

- Earnings were above expectations due to higher associate earnings. FY22 revenue and PATMI at 101%/109% of our FY22e forecasts. Associate earnings almost doubled from a gain on disposal and reversal of write-down on properties held for sale.

- Beer volumes recovered strongly post-lockdown in Vietnam. Total volumes jumped 54% YoY with EBITDA doubling. Final dividend up 20% YoY to Bt0.60 (S$0.023).

- We maintain our BUY recommendation with an unchanged target price of S$0.80. Our target is pegged at 18x FY23e earnings for the core operations, its 5-year average. And listed associates valued at market valuations. We expect FY23e to be a year of growth as the re-opening of borders and entertainment outlets resume; increased selling prices; and demand further spurred by multiple events including the World Cup and upcoming elections. Gross margins are expected to improve as commodity prices taper down but higher marketing spend will dampen the margin improvements.

The Positive

+ Surge in beer volume. Beer sales revenue rebounded with a 54% YoY jump in volumes following the lockdown in Vietnam. 4Q21 beer volumes were down almost 40% YoY. There were price increases in October 2022 for beer in Thailand and Vietnam; and longer drinking hours for the World Cup and 80% of on-trade premises re-opened will support sales in 1Q23. Distribution expenses will climb from increased marketing activities due to the return of more events.

The Negative

– Spirits volumes remain sluggish. Volumes in 4Q22 were flat at 139.9mn litres. Revenue improved from higher selling prices in white spirits. Brown spirit volumes are recovering from the re-opening of entertainment outlets and on-trade sales.

Source: Phillip Capital Research - 5 Dec 2022

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

RHB Investment Research Reports

ST Engineering - In-Line 9M24, Maintain Growth Expectations; Still BUY

2

3

CEO Morning Brief

4

CEO Morning Brief

Singapore Ends Pursuit of Money Launderers Who Forfeited US$1.4 Bil

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....