Trader Hub

United Overseas Bank Limited – Surge in Net Interest Margins

traderhub8

Publish date: Mon, 31 Oct 2022, 12:40 PM

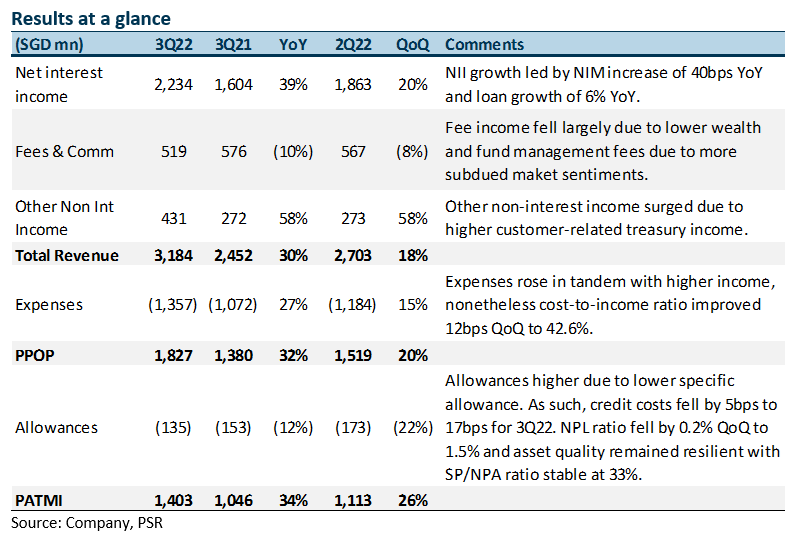

- 3Q22 earnings of S$1,403mn were in line with our estimates due to higher net interest margin (NIM) and healthy net interest income (NII) growth. 9M22 PATMI is 72% of our FY22e forecast.

- NII was up 39% YoY from a NIM increase of 40bps YoY to 1.95% and loan growth of 6% YoY. Fee income fell 10% YoY while other non-interest income was up 58% YoY. Management is guiding mid-single digit loan growth with higher NIMs, stable cost-to-income ratio and stable credit costs.

- UOB has guided NIM to continue to expand each quarter and to reach an exit NIM of 2.5% to 3.0% by the end of 2022. We estimate 4Q22 NII to jump 65% YoY. Management is guiding for ROE of 13% in FY23 and 14% for FY24 from this year’s 11%.

- Maintain BUY with an unchanged target price of S$35.70. We raise FY22e earnings by 6% as we increase NII estimates for FY22e. We assume 1.45x FY22e P/BV and ROE estimate of 12.1% in our GGM valuation. We raised FY23e earnings by 12% as we increased NII estimates for FY23e. Our ROE estimate for FY23e is raised from 11.5% to 12.7%. Every 25bps rise in interest rates can raise NIM by 0.04% and PATMI by 4.3%.

The Positives

+ NII increased 39% YoY, led by steady loan growth. NII grew 39% YoY, led by continued loans growth of 6% YoY, while NIM surged 40bps YoY to 1.95% (QoQ: 1Q22: +2bps, 2Q22: +9bps, 3Q22: +28bps). Loan growth QoQ was mainly from term and trade loans, while YoY loan growth was broad-based across Singapore, Greater China and the Western world as business regained momentum. UOB has maintained its guidance of mid-single digit loan growth for FY22e.

+ Other non-interest income increased by 58%. Other NII increased 58% YoY largely due to the higher customer-related treasury income. A similar QoQ increase of 58% was due to record high customer-related treasury income, as well as improved performance from trading and liquidity management activities amid market volatilities.

+ Credit costs improve due to lower SPs. Total allowances fell by 12% YoY to S$135mn resulting in credit costs improving by 3bps YoY to 17bps. This was mainly due to specific allowance decreasing by 18% YoY to S$127mn. Total general allowance for loans, including RLARs, was prudently maintained at 0.9% of performing loans. UOB has lowered its credit cost guidance to 20bps for FY22e (previously 25bps).

+ New NPAs fall 15% YoY. New NPA formation fell by 15% YoY and 68% QoQ to S$214mn as asset quality stabilised during the quarter. Resultantly, the NPL ratio fell by 0.2% QoQ to 1.5%. Asset quality remained resilient with SP/NPA stable at 33%. 3Q22 NPA coverage is at 98% and unsecured NPA coverage at 207%.

The Negatives

– Fee income continues to decline. Fees fell 10% YoY largely due to lower wealth and fund management fees. The decline of 8% QoQ was mainly due to loan-related fees moderating from last quarter’s high, while wealth management fees remained soft amid subdued market sentiment. However, loan-related fees continued to show stable growth of 5% YoY, spurred by trade and investment growth, while credit card fees were higher 6% YoY as customer spending rebounded with borders reopening.

– CASA ratio declined YoY. Current Account Savings Accounts (CASA) ratio fell 6% YoY to 49.8% mainly due to the high interest rate environment and a move towards fixed deposits (FD). Nonetheless, total customer deposits increased 6% YoY to S$375bn. Management has mentioned that they are concentrating on increasing FD campaigns and that the increase in FDs was higher than the drop in CASA.

Source: Phillip Capital Research - 31 Oct 2022

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

THE SINGAPOREAN INVESTOR

Investing in Singapore's Hospitality Scene: A Look at the 5 Listed REITs

2

RHB Investment Research Reports

Food Empire - Expanding Ingredients Capability in Vietnam; BUY

3

RHB Investment Research Reports

ST Engineering - Rolling Forward Our Valuation; Reiterate BUY

4

CEO Morning Brief

Singapore Home Sales Set for Worst Year Since Financial Crisis

5

SGX Market Dialogues

Kopi-C With GuocoLand’s Group CEO: ‘We Have Twin Engines for Growth’

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....