Trader Hub

Singapore Telecommunications Ltd – Re-opening and Restructuring Upside

traderhub8

Publish date: Mon, 30 May 2022, 05:01 PM

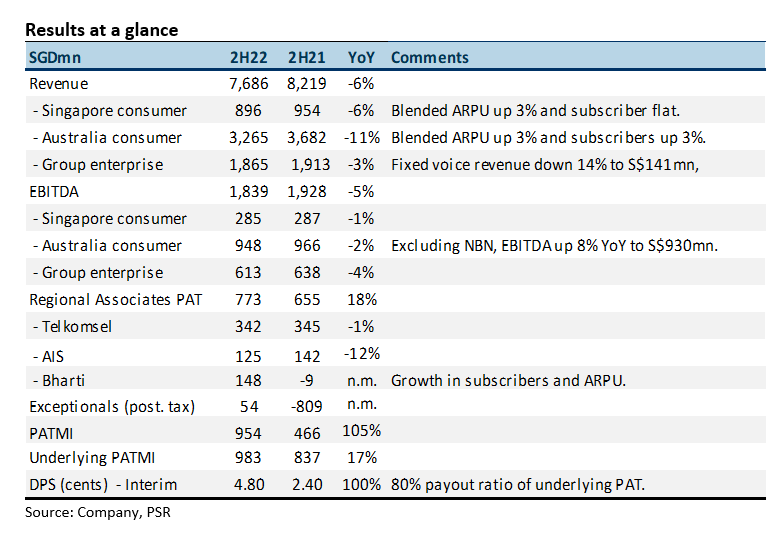

- FY22 revenue met our expectations at 101% of FY22e estimates. EBITDA was 93% of estimates due to lower-than-expected NBN migration earnings.

- 2H22 EBITDA was down 5% YoY, the largest drag from NCS and widening losses in Trustwave. Underlying PAT in 2H22 was up 15% excluding exceptional items, NBN and job support scheme.

- We lower our FY23e forecast by a modest 2% to account for weaker enterprise earnings. Our SOTP TP is raised from S$2.86 to $3.05 as we roll over our EV/EBITDA into FY23e and higher associate market valuations. Earnings in FY23e are expected to recover as roaming revenue creeps up and economic conditions improve in emerging countries post lock-down. The targeted monetization of around S$3bn assets will help narrow the valuation discounts for associates, strengthen the balance sheet and improve the capacity to raise dividends. Some of the assets identified for recycling of capital include disposal of Amobee, redevelopment of Comcentre and possibly part disposal of associate stakes. We maintain our ACCUMULATE recommendation.

The Positives

+ Improving earnings in Australia. Mobile service revenue rose 4% YoY to A$1.84bn, supported by both ARPU and subscriber growth. Optus mobile plans are gaining traction with customers for their more differentiated offering in terms of 5G speed, on-demand product features and improvement in customer service levels. Total consumer revenue in Australia declined due to a drop in NBN migration revenue (-83% YoY) and slower equipment sales (-25% YoY).

+ Huge reversal in Bharti earnings. The growth in earnings was driven by a 23% rise in ARPU and a 12% increase in 4G subscribers in India. Airtel Africa also delivered a 24% improvement in EBITDA through subscribers (+9%) and ARPU growth (+11%).

The Negative

– Sluggish enterprise and NCS earnings. EBITDA fell 4%, dragged down by a 14% drop in fixed voice revenue and 3% fall in leased circuits and broadband. Excluding JSS, NCS recorded a 4% rise in EBITDA. Margins were softer due to a 19% YoY rise in staff costs.

Outlook

Key drivers to earnings recovery in FY23e are 1) Roaming revenue in Singapore consumer and enterprise; 2) Organic and inorganic growth in NCS; 3) Economic recovery post-lockdown in emerging markets of Thailand, Philippines and Indonesia; 4) Improving ARPU in India and rising data traffic.

Source: Phillip Capital Research - 30 May 2022

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

THE SINGAPOREAN INVESTOR

Investing in Singapore's Hospitality Scene: A Look at the 5 Listed REITs

2

RHB Investment Research Reports

Food Empire - Expanding Ingredients Capability in Vietnam; BUY

3

RHB Investment Research Reports

ST Engineering - Rolling Forward Our Valuation; Reiterate BUY

4

CEO Morning Brief

Singapore Home Sales Set for Worst Year Since Financial Crisis

5

SGX Market Dialogues

Kopi-C With GuocoLand’s Group CEO: ‘We Have Twin Engines for Growth’

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....