Trader Hub

City Developments Limited – Promising Turnaround

traderhub8

Publish date: Mon, 14 Mar 2022, 09:13 AM

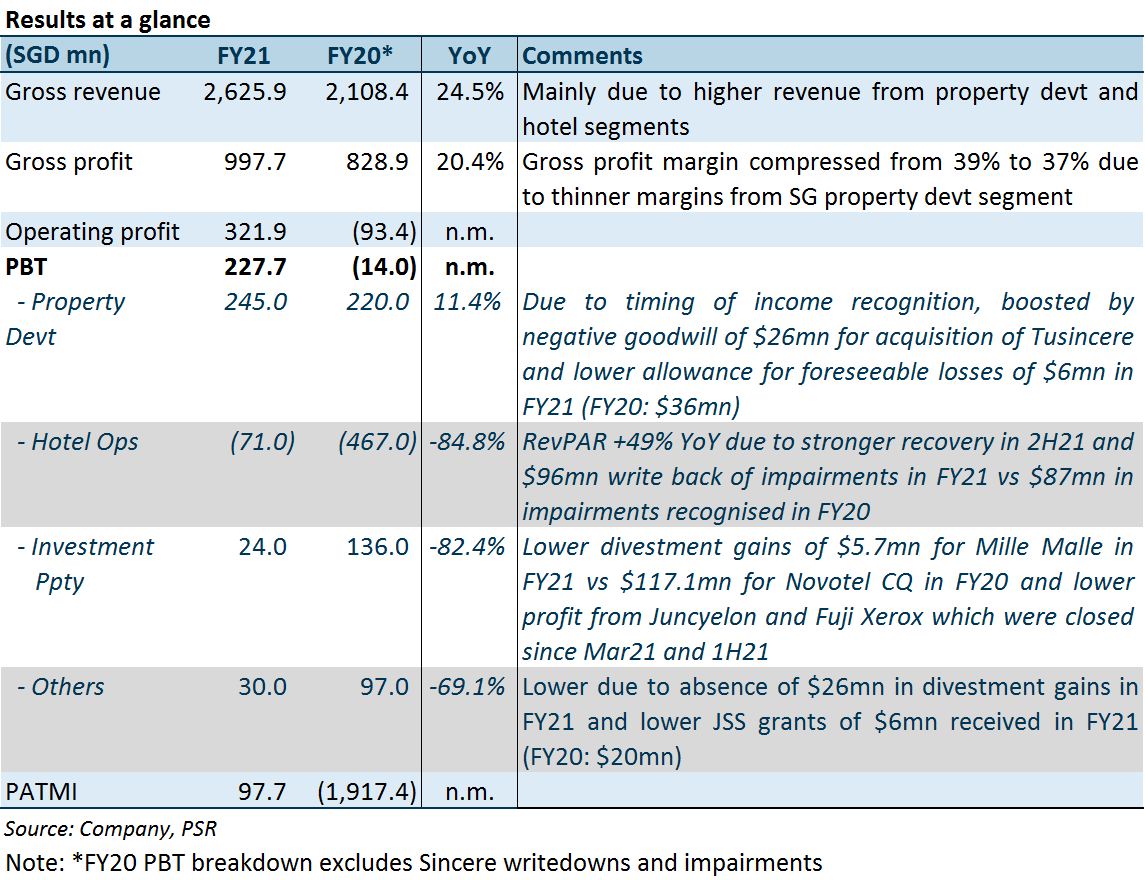

- FY21 revenue of S$2,626mn (+24.5% YoY) formed 106% of our forecast but PATMI underperformed due to higher-than-expected taxes, excluding which, performance would have been in line with our forecasts.

- PATMI in the black due to strong residential sales and recovery in the hospitality segment, which has turned EBITDA positive. CDL moved 2,185 units in FY21, exceeding our sales forecast of 1,600 units.

- Proposed DPS of 31.1 Scts (FY20: 12 Scts), comprising 12 Scts in cash and a surprise distribution in specie of CDL Hospitality Trust (CDREIT SP, not rated) valued at 19.1 Scts.

- Maintain BUY and RNAV-derived TP S$9.19 (35% discount). We view CDL as proxy for the Singapore residential market and hospitality recovery play. CDL is trading at an attractive 48% discount to our RNAV/share of S$14.14. Asset monetisation, unlocking value through AEIs and redevelopments, and faster-than-expected recovery in hospitality portfolio are potential catalyst for CDL, which could help narrow the discount between CDL’s share price and RNAV.

The Positives

- Highest number of residential sales in 10 years. CDL sold 2,185 units in Singapore with total sales value of S$4.3bn in FY21. This was 66% and 131% higher than FY20’s 1,318 units and total sales value of S$1.8bn and surpassed our FY21 sales estimate of 1.6k units. This was attributed to strong take-up at two projects, Irwell Hill Residence and CanningHill Piers, which were launched in FY21 and are presently 77% and 86% sold. However, due to higher land and development cost for newer projects, PBT margin for the development segment compressed from 23% to 22%.

- Hotel segment turned EBITDA positive. RevPAR jumped 49% YoY, with significant pick-up observed in 2Q/3Q21. Portfolio occupancy improved YoY from 38.6% to 51.0%, widening gross operating margin from 3.7% to 21.8% (2019: 39%). Hotels in US and Europe recovered faster than those in Asia and Australia which experience longer periods of lockdowns and restrictions. Hospitality EBITDA still 40% below 2019 levels. More recovery expected as travel returns.

- Opportunistic divestment of Millennium Hilton Seoul and Tanglin Shopping Centre. CDL signed a Sale and Purchase Agreement (SPA) to divest Millennium Hilton Seoul for S$1.25bn on 24 Dec 2021. The sales was completed on 24 Feb 2022 with significant divestment gain of S$528.8mn to be booked in FY22. CDL also launched a public tender for Tanglin Shopping Centre in December 2021, which closed on 22 February 2022 with a top bid of S$868mn or S$2,769 psf ppr. CDL owns 60% of NLA in this strata-titled property and we estimate this could unlock c.S$280mn in divestment proceeds for the group, which will be booked in FY22.

The Negative

- Listing of UK commercial REIT delayed. The listing of a UK commercial REIT, of which CDL would be the co-sponsor, was intended for 2021 but did not materialise. The management intends to continue the listing process. While the delay in listing was a setback, occupancy of the two assets that will be injected into the REIT, 125 Old Broad Street and Aldgate House, has improved. This should strengthen the initial portfolio for the upcoming UK Commercial REIT. As per our estimates, assuming a 20-25% stake for CDL, the injection of 125 Old Broad Street and Aldgate House into a 38%-geared S$3.5bn SREIT portfolio could unlock S$526-633mn for the group.

Outlook

Healthy inventory levels allow for more conservative bidding

Three residential launches totalling 1,291 units are in the pipeline for 2022. CDL also picked up two more sites which will add 1,048 units to the pipeline, bringing unsold inventory to 3,047 as at 31 Dec 2021. CDL’s inventory levels are healthy, allowing it to be more selective and conservative when bidding for new sites. The site at Upper Bukit Timah Road was purchased in an off-market deal from Tan Chong Realty for S$126.3mn or S$603 psf and could yield 603 units. On 26 Jan 2022, CDL won the tender for the Jalan Tembusu GLS with a bid of S$589.9mn or S$1,302 psf, adding 640 units to the pipeline. Given the higher land prices and cost of construction, CDL is aiming for margins of at least 10% for new projects.

Unlocking value through strategic redevelopments

CDL entered into a put and call option agreement with Far East Hospitality REIT (FEHT SP, not rated) to acquire Central Square, a 99-year leasehold commercial and residential development, with a remaining lease tenure of approximately 72 years, for S$315mn. Central Square is adjacent to CDL’s Central Mall. The purchase of Central Square is expected to be completed in Mar22. The enlarged site, comprising Central Mall’s office component, Central Mall conservation shophouses and Central Square, will be redeveloped under URA’s Strategic Development Incentive Scheme, yielding a GFA uplift of 67%, from 441,650 sq ft presently to 735,00 sq ft. The proposed mixed-use development will comprise commercial, hotel and service apartment components, subject to CDL getting planning approval for residential use. Phased completion for this redevelopment is expected in 2027.

City House, which is located along Robinson Road and Cross Street, falls under the CBD Incentive Scheme, which could potentially unlock additional GFA. Similar to the Fuji Xerox redevelopment, the redeveloped site could benefit from GFA uplift if CDL decides to undertake the redevelopment to convert the assets into a mixed-use development. The management is currently evaluating the merits of undertaking a redevelopment and has not announced any plans presently.

Distribution in Specie hints at more active recycling of hospitality assets

CDL has proposed distribution in specie (DIS) of CDLHT valued at 19.1 Scts, allowing shareholders to take park in the recovery of the hospitality sector. The DIS will reduce CDL’s stake in CDLHT from 38.7% to 27%, resulting in a deconsolidation of CDLHT. CDL will recognise an estimated accounting gain of c.S$467.5mn on the deconsolidation of CDLHT and gearing will improve from 61% to 55% on a pro forma basis. The deconsolidation will allow CDL to recognise gains on any future sale of assets to CDLHT should the transaction value exceed the carrying book value of the assets while allowing unitholders to benefit from the recovery in the hospitality sector. This could be the start of more active recycling of hospitality assets to CDLHT. The DIS will be subjected to shareholder approval during the AGM on 28 April 2022.

Maintain BUY and RNAV TP of S$9.19

We view CDL as proxy for the Singapore residential market and hospitality recovery play. While land prices have trended up in recent years, redevelopment and off-market purchases should provide better margins, allowing to replenish its inventory and participate in the peaking Singapore residential market. CDL is trading at an attractive 48% discount to our RNAV/share of S$14.14. Asset monetisation, unlocking value through AEIs and redevelopments, and faster-than-expected recovery in hospitality portfolio are potential catalyst for CDL, which could help narrow the discount between CDL’s share price and RNAV.

Source: Phillip Capital Research - 14 Mar 2022

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

2

3

Johor house best buy

4

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....