Trader Hub

Sheng Siong Group Ltd – New High in Gross Margins

traderhub8

Publish date: Fri, 25 Feb 2022, 06:55 PM

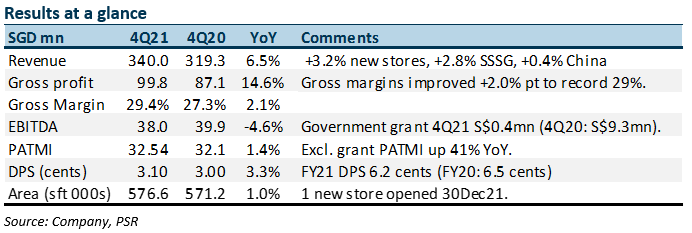

- FY21 revenue/PATMI beat our estimates at 102%/105% of our forecast. Gross margins were stronger than expected. Excluding grants, PATMI would have risen 41% YoY.

- Improvement in the product mix of higher fresh food and house brands drove the expansion in margins. Households continue to dine at home and shift their fresh food purchases from wet markets to supermarkets.

- Our FY22e PATMI is increased by 13% to S$114.7mn as we lift sales estimates by 12%. We believe the secular trend of fresh food sales migrating from wet markets to supermarkets continues. Our BUY recommendation is maintained and target price is nudged up to S$1.75 (prev. S$1.69). We lower our valuation metrics to 23x PE, a 10% discount to 5-year historical average of 25x PE. Earnings growth will be capped until new stores contribute meaningfully, likely in FY23e. FY22e will be a transition year as household dining may soften as borders reopen, dining restrictions lift and more return to office.

The Positive

+ Gross margins still climbing. Margins hit another record high of 29.4% (3Q21: 29.0%). Supporting margins was the higher mix of fresh food and house brands. We believe the disruption last quarter in fresh food supplies diverted even more customers to Sheng Siong. Awareness is growing on the quality and price competitiveness of fresh food compared to wet markets. A similar experience is underway for house brands where more SKUS are being added particularly in the frozen category.

+ Three new stores secured. After almost five quarters without a new store, Sheng Shiong managed to open a new 5,500 sft store in Bukit Batok. Another two more stores, totalling 19,000, sft are expected to open in FY22. This will raise Sheng Siong’s total store footprint in Singapore by 4.3%.

The Negative

– Nil

Outlook

We expect sales in FY22e to soften as borders reopen, dining restrictions lift and more return to office. Dining more at home also results in a larger budget for higher quality and pricier fresh products. We expect only a modest dip in gross margins. Sales from fresh products can creep up higher with further market share gains from wet markets. A headwind will be rising food cost and price competition.

Maintain BUY with higher TP of S$1.75 (prev. S$1.69)

SSG enjoys attractive ROEs of 27%, dividend yields at 3.7% and net cash at S$241mn (as at Dec2021).

Source: Phillip Capital Research - 25 Feb 2022

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

THE SINGAPOREAN INVESTOR

Investing in Singapore's Hospitality Scene: A Look at the 5 Listed REITs

2

RHB Investment Research Reports

Food Empire - Expanding Ingredients Capability in Vietnam; BUY

3

RHB Investment Research Reports

ST Engineering - Rolling Forward Our Valuation; Reiterate BUY

4

CEO Morning Brief

Singapore Home Sales Set for Worst Year Since Financial Crisis

5

SGX Market Dialogues

Kopi-C With GuocoLand’s Group CEO: ‘We Have Twin Engines for Growth’

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....