Trader Hub

BRC Asia – Strong Start to FY22

traderhub8

Publish date: Mon, 14 Feb 2022, 10:32 AM

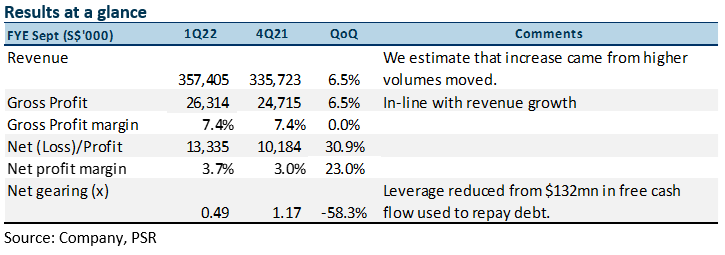

- 1Q22 net profit exceeded our expectations. We believe the beat came from higher volumes delivered. Orderbook stands at $1.3bn.

- Significant deleveraging of Group’s balance sheet as it saw a $132mn cash inflow for the quarter.

- The Building and Construction Authority (BCA) has upgraded forecasts of construction demand for 2022 by 3.5%. Steel rebar demand is forecasted to grow ~22% to 1mn-1.2mn tonnes in tandem with the overall construction sector recovery.

- Maintain BUY with an unchanged target price of S$1.84. Our TP is based on 11x FY22e P/E, still at a 15% discount to the 10-year historical average, on account of the uncertain environment. Catalysts expected from higher foreign-worker inflows to Singapore.

The Positives

+ 1Q22 net profit exceeded our expectations. In spite of the resurgence of COVID-19 in Singapore, we estimate that order deliveries went up as disruptions to construction schedules were minimised with more frequent testing. The 6.5% higher QoQ sales (from the Group’s voluntary update) also came as a surprise because of the seasonally weaker 1H of the financial year. Despite the strong beat, we are keeping our forecasts for FY22e unchanged as we monitor the overall recovery of the construction sector.

The Group’s order book inched up to $1.3bn from $1.2bn as the construction sector continues its recovery. We estimate that half of the order book will be fulfilled within the next 12-15 months.

+ Significant deleveraging of Group’s balance sheet. The Group benefitted from a free cash inflow of $132mn for the quarter, which was used to deleverage its balance sheet. We believe a significant portion of the cash inflow was used to repay the trade facilities that it takes on to procure steel raw materials.

Despite the lower gearing ratio in 1Q22, we still expect gearing for FY22e-23e to remain elevated as we forecast firmer steel prices in 2022. Even though steel prices corrected by about 30% late last year, they have since rebounded by ~19% underpinned by prospects of strong demand supported by China’s plans of infrastructure investment in a bid to boost economic stability.

Outlook

Easing border restrictions to aid further recovery in the construction sector. With higher vaccination rates (~88%), we believe the government will progressively loosen border restrictions to alleviate the tightness in the labour market. The number of seasonally adjusted job vacancies in the overall economy rose to an all-time high of 98,700 in September 2021. The number of vacancies is especially acute in sectors which rely most on foreign workers, such as construction and manufacturing. In the first half of 2021, the total number of foreign workers declined by 32,600. The seasonally adjusted job vacancy to unemployed person ratio rose to 2.09 in September 2021, from 1.63 in June 2021. We therefore believe the government will progressively facilitate the safe inflow of new foreign workers to alleviate the manpower crunch while ensuring that the risk of COVID-19 importation is well-managed to protect public health. The Ministry of Health recently announced the easing of measures for travellers from various countries, including Malaysia.

BCA upgrades forecasts of construction demand for 2022. The BCA has upgraded its forecasts of construction demand for 2022 to $27bn-32bn per year from the original $25bn-32bn per year, comparable with the preliminary $30bn in 2021. The BCA also projects that demand for building materials will increase in tandem with the increased construction demand. Steel rebar demand is forecasted to grow to 1mn-1.2mn tonnes in 2022, representing ~22% YoY increase.

We note that BCA’s forecasts for average construction demand in 2022-2025 excludes the development of Changi Airport Terminal 5 and expansion of the two integrated resorts. As our forecasts have not included these projects, there is upside if they go live.

In the near term, projects in the pipeline that will likely support the group’s growth are the Singapore Science Centre’s relocation, the Toa Payoh integrated development, Alexandra Hospital redevelopment, Bedok’s new integrated hospital, Phases 2-3 of the Cross Island MRT Line and the Downtown Line’s extension to Sungei Kadut.

With an approximately 65% market share in the reinforced steel industry, we continue to see BRC Asia as a key beneficiary of the construction sector recovery.

Source: Phillip Capital Research - 14 Feb 2022

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

2

3

Johor house best buy

4

CEO Morning Brief

5

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....