Trader Hub

CapitaLand Integrated Commercial Trust – Portfolio Reconstitution Amidst Recovery

traderhub8

Publish date: Fri, 04 Feb 2022, 04:29 PM

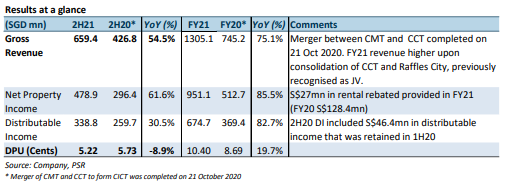

- FY21 DPU of 10.40 Scts (+19.7% YoY) was in line, forming 102% of our forecast.

- Operating metrics continue to improve; tenants’ sales lifted by broader recovery amongst trade sectors while negative retail reversions continue to narrow.

- Portfolio occupancy declined by 2.5ppts YoY due to timing of lease expiries at Capital Tower and Six Battery Road and trading impacted Clarke Quay.

- Maintain ACCUMULATE, DDM-based (COE 6.41%) TP lowered from S$2.54 to S$2.39. FY22e-26e DPU lowered by 5.2-6.7% to factor in higher utility and energy costs as well as the rising cost of borrowing. Our DDM-based TP dips from S$2.54 to S$2.39 on lower DPU estimates and higher cost of equity of 6.41% assumption (previous 6.27%). Catalysts for CICT include asset enhancement initiatives and acquisition.

The Positives

+ Recovery in tenant sales and narrowing negative reversions support improving tenant sentiment. Full-year retail reversions narrowed to -7.3% (1H21: -9.1%). Suburban and downtown reversions were -2.4% and -13.8% respectively. Tenant retention remains stable at 82% (FY20 84.5%). Broader recovery amongst trade categories was observed from the 12.2% YoY growth in total tenants’ sales, with nine out of 15 trade categories showing YoY growth. However, FY21 tenant sales psf was still below pre-pandemic levels, at 87.8% of FY19’s monthly average. Rental support has also eased – FY21 rental waivers came in at S$27mn, slightly more than half a month of rent, compared to the S$128.4mn in rebates disbursed in FY20.

+ Valuation uplift of 3.5% or S$752.8mn YoY. Retail assets saw a modest 3% valuation uplift on the back of recovering performance while cap rates remain unchanged. Office and integrated development assets accounted for 45% and 52% of the revaluation gains, owing to cap rate compressions for office assets and CapitaSpring achieving TOP in Nov 21. Clarke Quay and Raffles City took a S$52mn and S$107mn write-down due to CAPEX provisions for upcoming AEI works. Valuation for Gallileo fell by 13.2% of S$76mn as valuers factored in the exercise of lease break option by Commerzbank, which will bring forward the lease expiring from 2029 to 2024.

+ Portfolio reconstitution and entry into new market. CICT divested its 50% stake in OGS for S$640.7mn at an exit yield of 3.17%, 9.1% above valuation price on 30 Sep 21. It also entered a new market, Australia, making a A$1.1bn investment in two Grade A office buildings and 50% interest in integrated development, 101-103 Miller Street and Greenwood Plaza. These three Australian acquisitions carry an average NPI yield of 5.1% and a pro-forma DPU accretion of 2.8%. Post-acquisition, Australia represents c.5% of AUM. Capital recycling continued into FY22 – CICT announced the sale of JCube for S$340.0m at NPI yield of c.4%, 21.9% above FY21 valuation, realising net gains of S$56.7mn.

Source: Phillip Capital Research - 4 Feb 2022

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

2

3

Johor house best buy

4

CEO Morning Brief

5

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....