Trader Hub

StarHub Limited – Stable With Roaming + Cybersecurity Optionality

traderhub8

Publish date: Mon, 15 Nov 2021, 09:57 AM

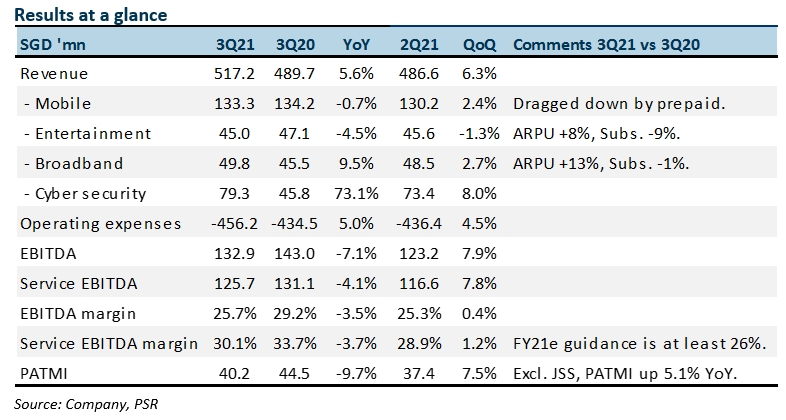

- 3Q21 results met our expectations. 9M21 revenue and EBITDA were at 72% and 80% of our FY21e forecasts respectively.

- Broadband and entertainment revenue trending ahead of our estimates due to increase in ARPUs. Mobile remains weak, dragged down by large churn in prepaid subscribers.

- 3Q21 cybersecurity operating profits more than doubled from S$2.8mn to S$5.8mn.

- No change to our forecasts. We maintain NEUTRAL with an unchanged target price of S$1.24. Valuations based on regional peers’ 6x FY21e EV/EBITDA. Starhub pays a stable 4% dividend yield with undervalued optionality in roaming and cybersecurity. There is upside to our target price if borders re-open faster, allowing roaming revenue to return. Another re-rating catalyst is sustained earnings from the cybersecurity operations or a corporate exercise for higher price discovery.

The Positives

+ Surge in operating profit in cybersecurity. 3Q21 revenue jumped 73% YoY to S$79mn. Operating profits spiked from S$2.8mn to S$5.8mn. The quarterly revenue run-rate improved from around S$40mn to S$70mn. There is revenue volatility due to project timing. But underlying demand is secular due to consistent threat intrusions, cyber-attacks and outsourcing of cybersecurity needs to established organizations such as Ensign.

+ Rising ARPU in broadband. ARPU jumped 13% YoY to S$34 on the back of reduced legacy promotions and higher 2GBps data plans with OTT bundles.

The Negative

– Mobile revenue is still soft. The loss of roaming revenue has capped postpaid ARPU at S$29, almost 30% below pre-pandemic S$40 (excluding the impact of SIM-only plans). This quarter experienced a huge 50k churn out of prepaid customers to 458k subscribers.

Outlook

Border re-opening especially in Malaysia and China will be key drivers for roaming revenue to return. Dividend guidance of a minimum of 5 cents per share or at least 80% PATMI is maintained.

Maintain NEUTRAL and TP of S$1.24

Our valuation remains based on regional peers’ 6x FY21e EV/EBITDA.

Source: Phillip Capital Research - 15 Nov 2021

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

2

3

Johor house best buy

4

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....