Trader Hub

ComfortDelGro Corp Ltd – Restructuring Whimper But Cash Rolling-in

traderhub8

Publish date: Mon, 15 Nov 2021, 09:57 AM

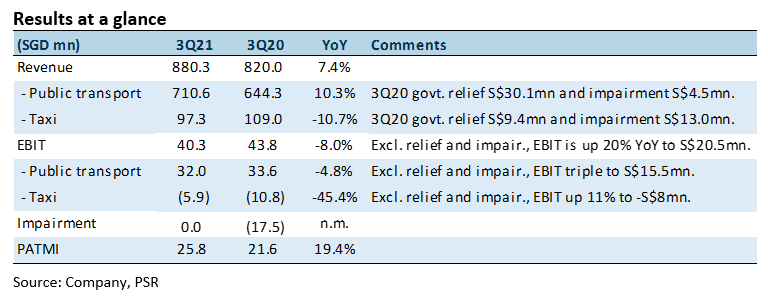

- 3Q21 earnings was below expectations. 9M21 revenue and PATMI was 70%/60% of our FY21e forecast respectively. Taxi rebates in 3Q21 resulted in operating losses.

- Downtown Line (DTL) transitioning to NRFF 2 resulted in a net S$15mn saving. But new bus contract extension may lower future operating earnings by S$34mn.

- The downside protection of earnings from NRFF 2 was lower than expected. At the peak of the restrictions last year, savings was only around S$15mn. Any shortfall in takings is limited to the license fee payable to authorities. We lower our FY21e PATMI by 8%. Our DCF target price (WACC 8%) is lowered modestly to S$1.80. The downside in revenue is offset by lower than expected capital expenditure. Operating cash-flows for the company remains healthy, coupled with record cash levels. Comfort is our transport proxy for Singapore’s reopening and normalisation of social and work activities.

The Positive

+ Healthy cash-flow. FCF generated during the quarter was around S$95.2mn (3Q20: S$137.7m). Net cash has bulked up to S$458mn (3Q20: S$116mn), including finance lease. Despite the weak operating performance, operating cash-flows has been healthy. 9M21, cash from operations is S$582mn (9M20: S$428mn). Capital expenditure is around S$200mn p.a. against the S$350mn pre-pandemic.

The Negatives

– Taxi rebate still bite. Due to the continuation of restrictions in Singapore, there was a rebate of 25% given in taxi rentals. It will continue until November. As a result, taxi operations suffered S$8mn operating losses in 3Q21 excluding government relief. Losses have widened from the S$2.1mn in the prior quarter.

Outlook

With social restrictions and borders still largely closed, we expect muted earnings for 4Q21. The transition to New Rail Financing Framework version 2 (NRFF 2) was a disappointment (Appendix 1). We had expected higher cover for the losses experienced in DTL. However, the losses are limited to service charge payable and computation of the shortfall was combined or offset with NEL and SPLRT. Furthermore, advertisement revenue has to be returned to the authorities.

Another negative surprise was the new bus contracts. Whilst the contract period has been extended, competition has driven down the service fee earned by S$34mn. It is not disclosed if the extension could drive economies of scale or savings in other areas. Details of the contract are not fully disclosed. Separately, the planned listing of the Australian subsidiary has been halted due to challenging market conditions.

Source: Phillip Capital Research - 15 Nov 2021

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

THE SINGAPOREAN INVESTOR

Investing in Singapore's Hospitality Scene: A Look at the 5 Listed REITs

2

RHB Investment Research Reports

Food Empire - Expanding Ingredients Capability in Vietnam; BUY

3

RHB Investment Research Reports

ST Engineering - Rolling Forward Our Valuation; Reiterate BUY

4

CEO Morning Brief

Singapore Home Sales Set for Worst Year Since Financial Crisis

5

SGX Market Dialogues

Kopi-C With GuocoLand’s Group CEO: ‘We Have Twin Engines for Growth’

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....