Trader Hub

NetLink NBN Trust - Some Growth Returning

traderhub8

Publish date: Mon, 08 Nov 2021, 06:36 PM

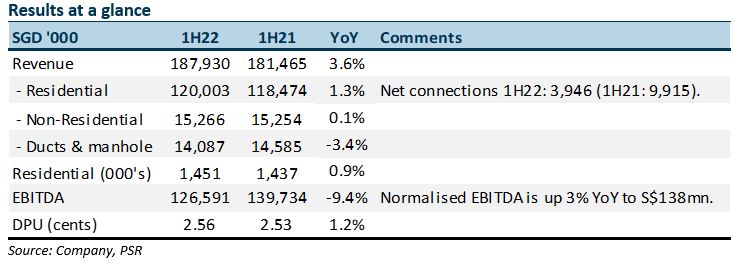

- 1H22 revenue and EBITDA were within expectations, at 50%/48% of our FY22e forecasts. DPU was raised a modest 1.2% YoY to 2.56 cents.

- 1H22 residential fibre connections rose only 3.9k. The run rate is below our 25k net connections expected in FY22e. Delays in the construction of new homes is the bottleneck.

- FY22e revenue estimate is nudged up for higher installation and diversion revenue. EBITDA is reduced by 5% to account for the one-off non-cash finance lease receivable remeasurement of S$12.4mn. Our DCF TP of S$1.03 (WACC 5.9%) and ACCUMULATE recommendation is unchanged. The dividend yield of 5.1% is expected to be stable, backed by monthly recurring revenue from more than 2mn fibre connections in homes and businesses.

The Positives

+ Normalised EBITDA expanded 3% YoY. Excluding the lease receivable remeasurement loss of S$12mn and grants and rebates last year of S$5.4mn, EBITDA is 1H22 would have risen 3.1% YoY to S$138mn (1H21: S$134.3mn). EBITDA growth came from the 38% revenue growth in diversion and co-location revenue to S$14mn. A rebound from last years circuit breaker disruption.

+ Lower interest expense. Finance cost was down 45% YoY to S$5.3mn. Borrowing cost has been lowered from 2.4% to 1.1% following the refinancing in June. Some of the hedges in the prior period has started to run off.

The Negatives

– Residential connections are still soft. New residential connections in 1H22 were only 3,946. A steep drop from 9,915 in 1H21. Our forecast for FY22e is lowered from 25,000 to 10,000 new connections.

Outlook

FY22e is a recovery from the circuit breaker disruption. Installation revenue from NBAP and diversion work rebounded from a low base last year. There is still a lingering impact from the pandemic due to delay in home construction, impacting residential connections. The increase in capital expenditure will depress dividends in the near term, but will build up the regulated asset base and yield returns in the next regulatory review

Our ACCUMULATE recommendation maintained on unchanged TP of S$1.03

NetLink’s dividend is stable with support from monthly recurring connection revenue and capital expenditure flexibility.

Source: Phillip Capital Research - 8 Nov 2021

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

THE SINGAPOREAN INVESTOR

Investing in Singapore's Hospitality Scene: A Look at the 5 Listed REITs

2

RHB Investment Research Reports

Food Empire - Expanding Ingredients Capability in Vietnam; BUY

3

RHB Investment Research Reports

ST Engineering - Rolling Forward Our Valuation; Reiterate BUY

4

CEO Morning Brief

Singapore Home Sales Set for Worst Year Since Financial Crisis

5

SGX Market Dialogues

Kopi-C With GuocoLand’s Group CEO: ‘We Have Twin Engines for Growth’

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....