Trader Hub

Venture Corporation Limited - Disrupted Quarter

traderhub8

Publish date: Fri, 05 Nov 2021, 05:25 PM

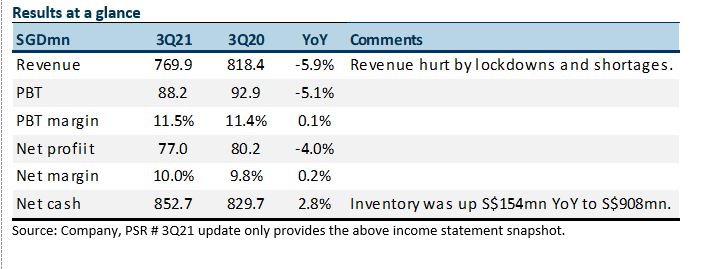

- Results were below forecast. 3Q21 PATMI declined 4% YoY to S$77mn. YTD21 Revenue and PATMI were 66% and 63% respectively.

- Fulfilment of customer orders disrupted by global components shortages and the Extended Movement Control Order (or factory closures) in Malaysia.

- We are lowering our FY21e revenue and PATMI by 6% and 10% respectively. Recovery this quarter has been stalled due to production disruptions. The company mentioned that demand is healthy and broad-based demand. In addition, the workforce in Malaysia is almost fully vaccinated, which should allow manufacturing activities to resume as normal. We expect some spill-over of orders into 4Q21. We maintain our NEUTRAL recommendation. Our target price is rolled over to 16x PE FY22e, its 5-year average. Re-opening and removal of lockdown should ease pressure on the supply chain in FY22e. The share price is currently supported by dividend yields of 4.5%, 11% ROEs and S$853mn net cash.

The Positive

+ Healthy balance sheet and margins. Net margins improved marginally to 10%. We assume the high-value low mix projects have been sustaining margins despite the weaker revenue and loss of operating leverage. Net cash was S$853mn at 3Q21. There was a spike in inventory by S$154mn YoY to S$908mn. We believe there is buffer inventory to cope with the unpredictability in component supply.

The Negative

– Another weak quarter in revenue. Pre-pandemic, the quarterly run-rate in revenue was around S$900mn. This has dropped to S$700m this year. Venture has struggled to keep revenues to pre-pandemic levels these past two years despite the global resurgence in electronics demand. The pivot to life science and consequent long timeline to ramp up is a factor, in our opinion. We expect revenue to rebound in 4Q21e to S$916mn, an 11% YoY rise.

Outlook

Venture commented that new product introductions are expected to flow to mass production over the next 12 months.

Maintain NEUTRAL with unchanged TP of S$19.20

Our FY21e and FY22e PATMI is lowered by 10% and 11% respectively

Source: Phillip Capital Research - 5 Nov 2021

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

2

3

Johor house best buy

4

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....