Trader Hub

Fortress Minerals Ltd – Hit by Production Disruptions

traderhub8

Publish date: Fri, 15 Oct 2021, 11:53 AM

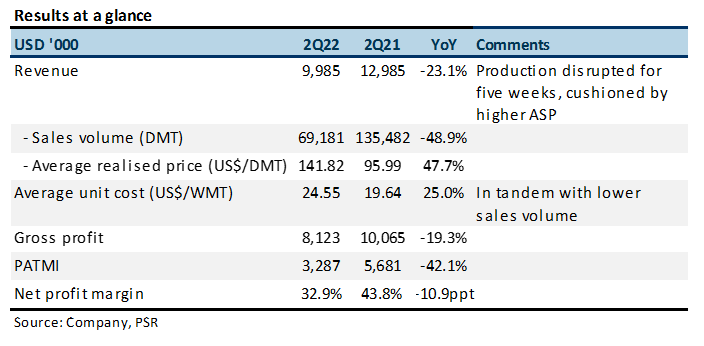

- 2Q22 results were below expectations. 1H22 revenue and PATMI at 39%/34% of our forecasts. Sales volume was lower than expected. ASP of US$141.82/DMT in line with our forecast of US$140/DMT.

- Production disruptions at Bukit Besi Mine during Phase 1 nationwide Total Lockdown under National Recovery Plan, which lasted for approximately five weeks.

- Downgrade to ACCUMULATE with lower TP of S$0.51. Our FY22e PATMI has been lowered by 22% to US$23.9mn as we decrease our sales volume forecast by 8.6% to 455,020 DMT. Iron ore prices are expected to remain weak around US$140/DMT, with continued steel production cuts in China. As such, we lower our ASP forecast to US$120/DMT for FY22e.

The Positives

+ Higher iron ore prices. 2Q22 revenue was down 23% YoY due to a 49% collapse in production. The 48% YoY improvement in selling prices offset some of the revenue weakness.

+ Operating cash flow increased. Operating cash flow catapulted from US$54k in 2Q21 to US$6.3mn in 2Q22, with the help of lower working capital. FCF turned positive to US$2.2mn, from US$495k, even with capex increasing to US$4.2mn, from US$549k.

The Negatives

– Lower sales volume. Sales volume was negatively impacted by the production disruptions at Bukit Besi Mine. Mining and processing activities have since resumed on 5 July 2021 at 80% capacity. Average unit cost rose due to the fall in production.

– Higher net debt. Bank borrowings increased from US$166k to US$22.9mn for the acquisition of Fortress Mengapur which was completed in April 2021 and purchase of equipment. Net debt increased further to US$14.7mn since 1Q22.

Updates

FML announced on 12 October 2021 that its subsidiary, Fortress Resources Pte Ltd, has entered into a new offtake agreement with a third-party domestic steel mill in Malaysia. Fortress Resources will deliver 375,000 WMT of iron ore to this customer over a 15-month period from 11 October 2021 to 31 December 2022 (3QFY22 to 4QFY23). The total volume of iron ore concentrate delivered in FY21 was 497,369 WMT.

Source: Phillip Capital Research - 15 Oct 2021

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

THE SINGAPOREAN INVESTOR

Investing in Singapore's Hospitality Scene: A Look at the 5 Listed REITs

2

RHB Investment Research Reports

Food Empire - Expanding Ingredients Capability in Vietnam; BUY

3

RHB Investment Research Reports

ST Engineering - Rolling Forward Our Valuation; Reiterate BUY

4

CEO Morning Brief

Singapore Home Sales Set for Worst Year Since Financial Crisis

5

SGX Market Dialogues

Kopi-C With GuocoLand’s Group CEO: ‘We Have Twin Engines for Growth’

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....