Trader Hub

Singapore Banking Monthly – Outlook Stable

traderhub8

Publish date: Tue, 31 Aug 2021, 11:51 PM

- Singapore loans were up 3.5% YoY in June. Business loans were up for the ninth straight month, by 2.6%. Consumer loans were up for the 11th straight month, by 0.7% YoY, aided by housing.

- Dividends returned to pre-pandemic levels. Provisions should be sufficient to address any increase in non-performing loans during the current economic uncertainties

- Maintain OVERWEIGHT. Loans continued their strong recovery with the highest MoM growth recorded for the year as Singapore began to ease movement controls. We prefer DBS (DBS SP, ACCUMULATE, TP: S$32

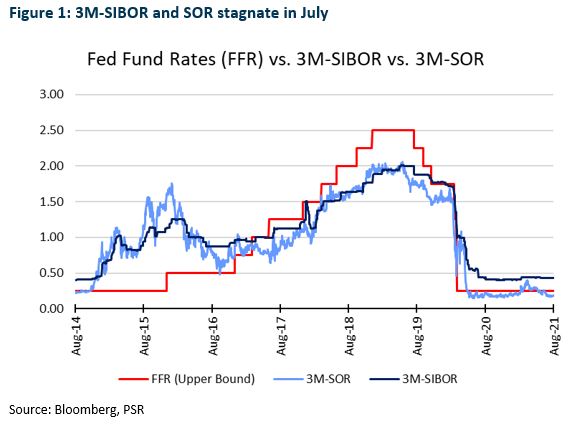

Local lending rates flat in July

Interest rates were flat in July, with 3M-SIBOR flat at 0.43% and 3M-SOR down 5bps to 0.19% as Singapore exited Phase 2 (Heightened Alert). Current 3M-SIBOR is 1bps lower than its 2Q21 average of 0.44%. 3M-SOR is 9bps lower than its 2Q21 average of 0.28% (Figure 1).

Banks resume pre-pandemic dividend payouts

After the MAS lifted restrictions on dividend distribution, all three local banks reverted to pre-pandemic DPS payouts. DBS paid 33 cents for 2Q21. UOB’s 1H21 DPS was 60 cents for a payout of 50%. OCBC declared an interim DPS of 25 cents for 1H21, representing a payout of 42%.

With the continued spread of the Delta variant in Southeast Asia and expiry of loan moratoriums, we expect a slight uptick in NPLs. We keep provisions for FY21e unchanged, however, as we believe sufficient provisions have been made.

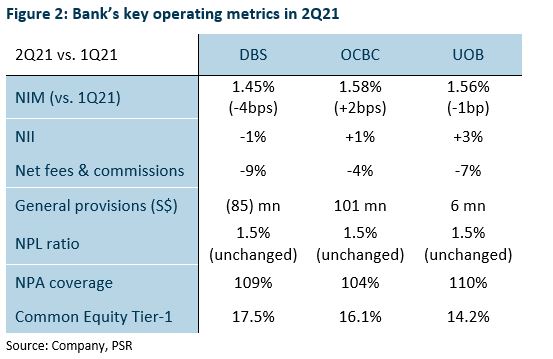

Stronger capital ratios and stable NIMs

DBS’ 2Q21 earnings were 10.7% above our 2Q21e forecast. The outperformance came from net fee income and S$85mn of GP reversals. NIMs retreated 4bps QoQ to 145bps. Full-year guidance is now at the lower end of guidance. Asset quality was stable, resulting in further GP write-backs of S$85mn. Management lowered full-year total allowances to under S$0.5bn (1H21 allowances at S$89mn).

OCBC’s 2Q21 earnings of S$1.16bn missed our expectation by 7% on higher-than-expected allowances. Allowances were largely for exposure to a large number of corporate customers in oil trading and offshore support vessels. Total allowances of S$232mn were made up of S$131mn SPs and S$101mn GPs. Nonetheless, NIM rose 2bps QoQ. As a result, NII edged up 1% QoQ. Provisions were higher than expected.

UOB’s 2Q21 earnings of S$1.0bn formed 25.5% of our FY21e forecast. Stronger-than-expected net fee and commission income offset lower trading and investment income. NIMs eased 1bp QoQ to 1.56%, though NII grew 3%, led by steady growth in term and trade loans in Singapore, North Asia and Rest of World.

Highest loans growth recorded for the year

Domestic loans rose 3.5% YoY in June, tracking above our expected range of 2- 3% for 2021 as fears of a slowdown from Singapore’s move to Phase 2 (Heightened Alert) did not materialise.

Business loans were up for the ninth straight month, by 2.6% YoY in June. Loans picked up 1.9% MoM. Loans to the building and construction segment, the single largest business segment, contracted 0.7% QoQ to S$151.33bn, though they still grew 2.2% YoY. Loans to manufacturing increased for the second straight month, by 1.8% YoY.

Consumer loans were up 0.7% YoY in June, for the 11th straight month. This was aided by strong loan demand in the housing segment. Housing loans, which make up three-quarters of consumer lending, extended their growth streak for the 10th straight month, up 3.4% YoY to S$206.3bn.

Overall loans through the domestic banking unit – which captures lending in all currencies but reflects mainly Singapore-dollar lending – rose for the eighth consecutive month, the strongest in the year. They were up 1.5% in June to S$703.9bn, vs. a 0.2% increase in May.

Source: Phillip Capital Research - 31 Aug 2021

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

2

3

Johor house best buy

4

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....