Trader Hub

UG Healthcare Corporation Ltd – Limited Selling Price Visibility

traderhub8

Publish date: Tue, 31 Aug 2021, 11:50 PM

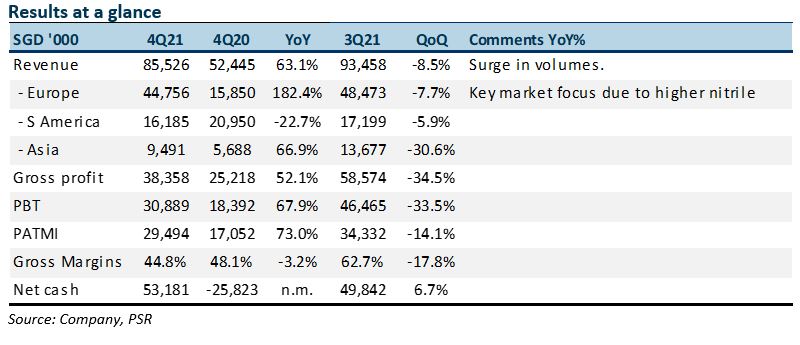

- 4Q21 results within expectations. FY21 revenue/PATMI at 101%/103% of our FY21e forecasts.

- Glove selling prices are falling as distributors and customers wind down their existing stocks. Falling prices make buyers hesitant to commit to purchases.

- We estimate industry selling prices for FY22e could drop by 40% YoY to around US$50. There is limited visibility on where selling prices will stabilise. FY22e PATMI is cut by 35% to S$49mn. Target price still pegged at a 30% discount to the Big 4 glove makers. This implies 8x FY22e PE and a target of S$0.63, down from S$0.85 previously. Recommendation downgraded to ACCUMULATE. Catalysts expected from stabilising selling prices but limited visibility currently.

The Positive

+ New capacity installed in April 2021. A 20% expansion in capacity to 3.4bn pieces of gloves was completed in April 2021. However, production was affected by temporary plant shutdowns due to Malaysia’s enhanced movement control order for factories located in Seremban.

The Negative

– QoQ weakness in earnings. Since peaking in 3Q21, we believe industry nitrile glove selling prices declined around 20% to US$80 in 4Q21. This brought down revenue and earnings QoQ.

Outlook

Industry glove selling prices have fallen from US$80 in 4Q21 to likely US$60 in 1Q22e. We do not expect prices to improve even in 2Q22e. Customers are hesitant to stock up, fearful of inventory losses as prices spiral downwards. Prices could deteriorate more as Malaysian manufacturers’ production recovers from the COVID-19 mandated shutdowns and cuts in utilisation. Chinese manufacturers are another source of disruption, with their aggressive expansion in nitrile capacity.

The positive for UG Healthcare is an expansion in effective capacity of at least 20% in FY22e. There would be another 35% jump in effective capacity to 4.6bn gloves in FY23e. Improved scale brings down production costs. Exposure to latex gloves and emerging markets could also offset falling nitrile glove prices, especially in developed markets.

Source: Phillip Capital Research - 31 Aug 2021

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

THE SINGAPOREAN INVESTOR

Investing in Singapore's Hospitality Scene: A Look at the 5 Listed REITs

2

RHB Investment Research Reports

Food Empire - Expanding Ingredients Capability in Vietnam; BUY

3

RHB Investment Research Reports

ST Engineering - Rolling Forward Our Valuation; Reiterate BUY

4

CEO Morning Brief

Singapore Home Sales Set for Worst Year Since Financial Crisis

5

SGX Market Dialogues

Kopi-C With GuocoLand’s Group CEO: ‘We Have Twin Engines for Growth’

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....