Trader Hub

NetLink NBN Trust – Fibre Connections Modestly Weaker

traderhub8

Publish date: Mon, 30 Aug 2021, 11:50 PM

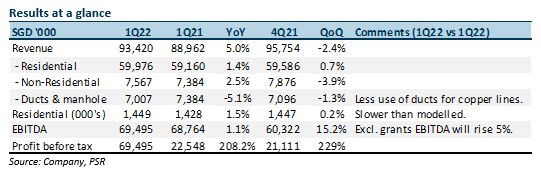

- 1Q22 revenue and EBITDA within expectations, at 25%/19% of our FY22e forecasts.

- Residential fibre connections increased by 2.3k this quarter, below our annual estimate of 25k. We expect a rebound in the latter part of FY22 with renewed home construction.

- No change in our estimates. ACCUMULATE rating and DCF TP of S$1.03 (WACC 5.9%) unchanged. Yields of 5.2% supported by monthly recurring revenue from more than 2mn fibre connections in homes and businesses. Regulatory review of fibre rates expected in mid-2022, likely implemented at end-2022.

The Positive

+ Non-residential connections highest in six quarters. Non-residential connections rose around 490 to 48.6k, the biggest increase in six quarters. The improvement came from higher take-up by small-medium enterprises. Non-residential is stable, around 8% of revenue.

The Negatives

– Run-rate of residential connections below our model. We are expecting 25k new residential connections in FY22e. 1Q22 new connections were only 2.3k. We expect improvements in 2HFY22 as HDB construction gathers pace. The 25k net additions represented a 1.7% increase to 1.44mn.

– Ducts and manholes remained weak. Revenue from ducts and manholes declined 5% YoY to S$7mn. The weakness could persist as major customer SingTel (ST SP,ACCUMULATE, TP S$2.52) will have less use of these ducts for copper-wire installations.

Outlook

FY22e should be a stable year for earnings and cash flows, supported by a large installed base of fibre connections. A 5-year regulatory review of prices will take place next year. There is limited visibility at present but fibre price charges may be moderately lower due to a decline in WACC and a higher base of connections. Offsetting this would be NetLink’s larger regulatory base and lower capex. Both should keep FCF at around S$200mn to sustain dividends.

Maintain ACCUMULATE and TP of S$1.03

NetLink’s key attribute is stable dividend yields backed by monthly recurring revenue from more than 2mn fibre connections in homes and businesses.

Source: Phillip Capital Research - 30 Aug 2021

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

RHB Investment Research Reports

ST Engineering - In-Line 9M24, Maintain Growth Expectations; Still BUY

2

RHB Investment Research Reports

3

CEO Morning Brief

Keppel DC REIT Buys Data Centres in Singapore’s Genting Lane for S$1b

4

5

CEO Morning Brief

Marina Bay Sands Eyes Singapore’s Largest Loan of US$9b — Bloomberg

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....