Trader Hub

Koda Ltd – Waiting for Resumption

traderhub8

Publish date: Mon, 30 Aug 2021, 11:50 PM

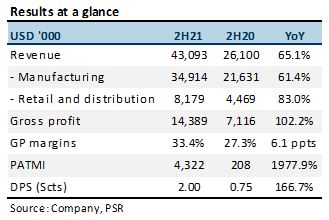

- 2H21 results beat, with FY21 revenue and PATMI at 116%/107% of our forecasts. The outperformance came from higher-than-expected manufacturing sales.

- 2H21 revenue grew 65% YoY while PATMI jumped 20x, from higher export sales, increased contributions from retail and distribution and improved gross margins.

- Maintain BUY with lower TP of S$1.10, down from S$1.32 as we roll over our 7x ex-cash P/E to FY22e. This is at the higher end of its historical 5-year ex-cash P/E. We lower FY22e PATMI by 29% to US$7.0mn. FY22e revenue estimate is largely unchanged but we cut gross margins from 32.0% to 29.5% for Covid-19 production disruptions at Koda’s plants in Vietnam and Malaysia. Catalysts still expected from higher exports to US and increase in production capacity.

The Positives

+ 2H21 revenue and PATMI increased. Higher revenue was led by higher export sales to all regions, especially North America, where sales surged 81% YoY to US$26.9mn. Retail and distribution sales also improved. The segment turned around from a net loss of US$835k in 2H20 to a net profit of US$217k in 2H21.

+ Improved margins. Gross margins increased 6.1 ppts YoY to 33.4%, following improved factory efficiency with higher production volume, which lowered unit production costs.

The Negative

– FY21 operating cash flow decreased 11.7% YoY to US$7.6mn. Both operating and free cash flow declined, the former due to higher working capital as inventories increased 72.5% to US$19.6mn and the latter due to capex which increased more than 2.5x to US$3.5mn, with the acquisition of a land use right and factory building in Vietnam for US$4.5mn.

Outlook

US furniture imports. Year to June 2021, US furniture imports increased 46.1% YoY to US$30.2bn. Even though imports in June 2021 dipped 1.5% MoM, they increased 55.6% YoY to US$5.3bn and were still above pre-Covid levels. We expect export sales to continue growing on the back of work-from-home with renewed virus-containment efforts.

Source: Phillip Capital Research - 30 Aug 2021

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

2

3

Johor house best buy

4

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....