Trader Hub

ComfortDelGro Corp Ltd – Clearer Recovery Path

traderhub8

Publish date: Thu, 19 Aug 2021, 10:46 AM

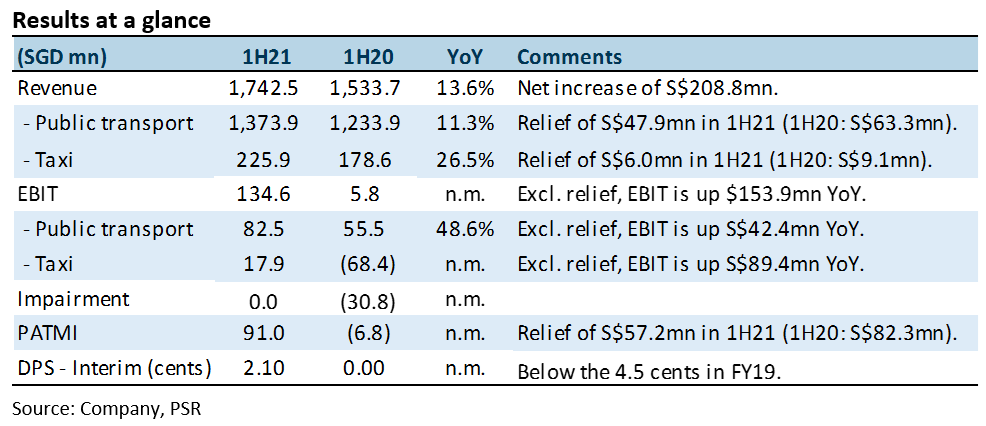

- 1H21 results within expectations. Revenue and PATMI of S$1,742mn/S$91mn form 46%/46% of our FY21e estimates. Earnings include government relief of S$57.2mn.

- Largest turnaround in taxi division. EBIT improved S$89.4mn in 1H21 despite continued rental discounts. Taxi rental rebates in Singapore of 20% in 1Q21 rose to 35% in 2Q21 due to Phase 2HA.

- Singapore is transitioning to endemic COVID-19. This implies an end to lockdowns as vaccinations make good progress. Our FY21e forecasts are unchanged. DCF target price (WACC 7.7%) maintained at S$1.83. Comfort is our preferred transport proxy for Singapore’s reopening and normalisation. Balance sheet strengthened in past 12 months despite pandemic. Net cash of S$493mn in 1H21, up from S$73.8mn in 1H20.

The Positives

+ Operating leverage intact. Revenue rose S$208mn YoY to S$1.74bn. Due to the business’ large fixed costs, around three-quarters of the revenue increase or S$154mn immediately translated into higher earnings. Taxis benefited from lower rental discounts while public transport gained from higher rail ridership and fuel indexation.

+ Return of interim dividends. FCF in 1H21 was S$287mn, up from S$189.1mn in 1H20. Interim DPS of 2.1 cents represents a payout of 50%. This is still below the 4.5 cents and 66% paid out before the pandemic in 1H19. Capex will likely trend below pre-pandemic S$300mn levels as a programme to purchase hybrid taxis is in its last stages with 600-700 units left to be purchased.

The Negatives

– Nil.

Outlook

Operating leverage and end of lockdowns are earnings catalysts, in our view. Pre-pandemic revenue and operating profit in 1H19 were S$1.92bn and S$222mn respectively. These compares with current operating profits before government relief of S$77mn. Our FY22e forecastes assume a close-to-full recovery to pre-pandemic levels.

Source: Phillip Capital Research - 19 Aug 2021

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

THE SINGAPOREAN INVESTOR

Investing in Singapore's Hospitality Scene: A Look at the 5 Listed REITs

2

RHB Investment Research Reports

Food Empire - Expanding Ingredients Capability in Vietnam; BUY

3

RHB Investment Research Reports

ST Engineering - Rolling Forward Our Valuation; Reiterate BUY

4

CEO Morning Brief

Singapore Home Sales Set for Worst Year Since Financial Crisis

5

SGX Market Dialogues

Kopi-C With GuocoLand’s Group CEO: ‘We Have Twin Engines for Growth’

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....