Trader Hub

Singapore Telecommunications Ltd – Thanks Again, Airtel and A$

traderhub8

Publish date: Tue, 17 Aug 2021, 06:25 PM

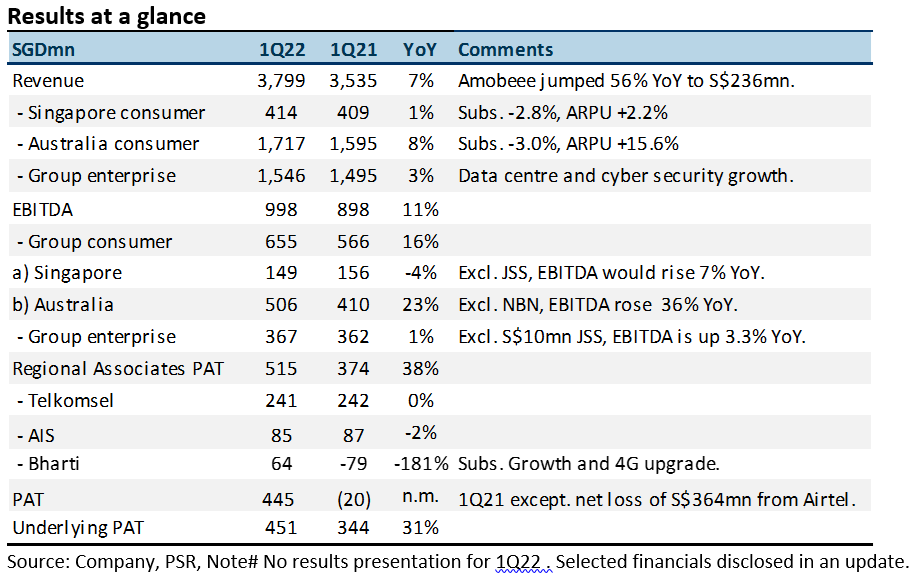

- 1Q22 revenue/EBITDA met our expectations at 25%/24% of FY22e estimates.

- Bharti Airtel’s (BHARTI IN, Not Rated) turnaround and an 11% YoY rise in A$ supported Optus earnings. We raise FY22e associate earnings by 6% to S$2bn.

- 1Q22 EBITDA for Australia consumer was better than expected on account of higher ARPUs. In comparison, EBITDA for enterprise was lower than modelled.

- Our FY22e EBITDA forecast is unchanged but PATMI raised by 4% with Airtel’s improvement. We upgrade Singtel to ACCUMULATE from NEUTRAL on the back of its recovery underway, led by Airtel, Bharti and later, border reopening, which should help to improve mobile revenue. SOTP TP raised to S$2.52 from S$2.32 with better associate valuations.

The Positive

+ Jump in Australia EBITDA. Mobile revenue was resilient, growing 5% YoY to A$1.26bn. EBITDA rose 23% YoY to S$506mn. Reasons mentioned were a cessation of fee waivers and rebates and lower bad-debt provisions. We believe the group’s S$305mn of impairments and payroll charges in 4Q21 also helped to lower its cost structure.

The Negative

– Enterprise growth was sub-par. Earnings growth in the enterprise segment has been below our expectations. Despite high demand from data centres and cyber security, legacy carriage business from voice and roaming remains a drag on earnings.

Outlook

The bright spots remain Airtel and Australia. We expect the corporate exercise at NCS and disposal of infrastructure assets to provide share-price catalysts in the short term.

Upgrade to ACCUMULATE with higher TP of S$2.52, from S$2.32

Our SOTP valuation is based on 6x EV/EBITDA for Singtel’s core Singapore and Australia businesses, at S$0.77/share. Associates are marked to market at S$1.75/share with a 20% discount to reflect volatility in their share prices.

Source: Phillip Capital Research - 17 Aug 2021

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

THE SINGAPOREAN INVESTOR

Investing in Singapore's Hospitality Scene: A Look at the 5 Listed REITs

2

RHB Investment Research Reports

Food Empire - Expanding Ingredients Capability in Vietnam; BUY

3

RHB Investment Research Reports

ST Engineering - Rolling Forward Our Valuation; Reiterate BUY

4

CEO Morning Brief

Singapore Home Sales Set for Worst Year Since Financial Crisis

5

SGX Market Dialogues

Kopi-C With GuocoLand’s Group CEO: ‘We Have Twin Engines for Growth’

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....