Trader Hub

IREIT Global – Occupancy-improvement and M&A Prospects

traderhub8

Publish date: Wed, 11 Aug 2021, 10:41 AM

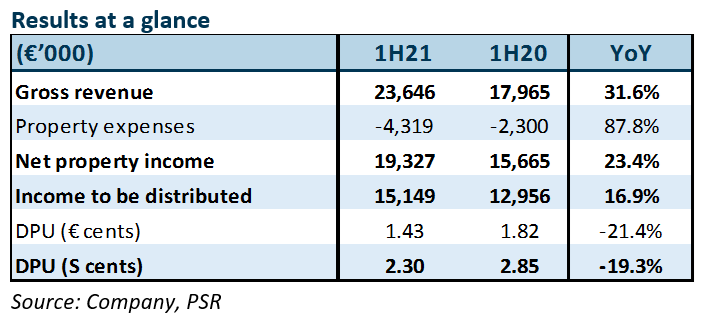

- 1H21 NPI and DPU in line, at 49.6%/51.7% of our FY21e estimates. No rent rebates or deferrals in 1H21. Portfolio valuation up by 3.9% HoH, led by a 7% increase for Berlin campus.

- Positive leasing in Germany and Spain to improve occupancy in 3Q21.

- We tweak FY21e DPU by 0.5% after a modest lift to revenue. Upgrade to BUY from ACCUMULATE with higher DDM TP of S$0.75, from S$0.68. Cost of equity lowered from 7.85% to 7.3% to reflect resilience of European office asset class. Catalysts expected from potential occupancy improvements and M&As.

The Positives

+ Stable. 1H21 NPI and DPU were in line, at 49.6%/51.7% of our FY21e estimates. Gross revenue and NPI increased 31.6% and 23.4% YoY following its acquisition of a remaining 60% interest in the Spanish portfolio on 22 October 2020. Property expenses jumped as its Spanish properties are multi-let and have lower NPI yields. DPU fell 21.4% YoY from an enlarged unit base following IREIT’s rights issue on 18 September 2020 There were no requests for rental rebates or deferrals from tenants in 1H21 – a good sign.

+ Higher valuations. Portfolio valuation was raised by 3.9% HoH, led by a 7% HoH increase for IREIT’s largest property, Berlin campus. Apart from lower discount and capitalisation rates applied across its portfolio, Deutsche Rentenversicherung Bund, its major tenant at the Berlin campus, did not exercise its break option in June 2021 to return part of its leased space to IREIT in 2022. As a result, its entire lease will now only expire in June 2024, raising Berlin campus’ income visibility. This bumped up the property’s valuation.

The Negative

– Nil.

Source: Phillip Capital Research - 11 Aug 2021

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

Trade Confidently & Analyze Charts Conveniently - Download VCPlus IOS & Android App Now!

Latest Videos

Apps

Top Articles

1

THE SINGAPOREAN INVESTOR

Investing in Singapore's Hospitality Scene: A Look at the 5 Listed REITs

2

RHB Investment Research Reports

Food Empire - Expanding Ingredients Capability in Vietnam; BUY

3

RHB Investment Research Reports

ST Engineering - Rolling Forward Our Valuation; Reiterate BUY

4

CEO Morning Brief

Singapore Home Sales Set for Worst Year Since Financial Crisis

5

SGX Market Dialogues

Kopi-C With GuocoLand’s Group CEO: ‘We Have Twin Engines for Growth’

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....