Trader Hub

Venture Corporation Limited – Modest Rebound

traderhub8

Publish date: Tue, 10 Aug 2021, 10:40 AM

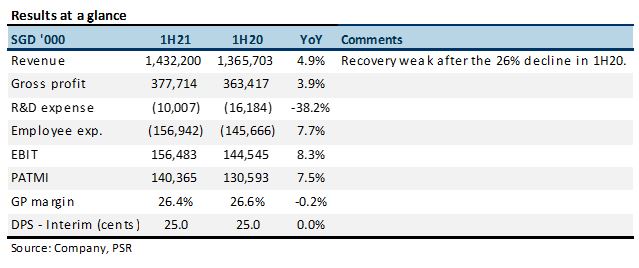

- 1H21 PATMI rose 7% YoY. Earnings were below at 40% of our FY21e estimate. Interim DPS unchanged at 25 cents.

- Rebound from last year’s supply-chain disruptions did not materialise. 1H21 revenue around 22% below pre-COVID levels.

- Earnings growth has stalled since peaking in FY17/18. Our earnings estimates are unchanged as we look forward to a pick-up in order momentum and operating leverage from life science, instrumentation and medtech in 2H21. Maintain NEUTRAL with unchanged target price of S$19.20, still at 16x FY21e P/E, its 5-year average. Support from decent yields of 4.4%, 10% ROEs and S$922mn net cash.

The Positive

+ Rock-solid balance sheet. Despite a need to raise inventories by S$103mn to S$766mn, net cash rose to S$922mn as at June 2021. This was an improvement over the S$833mn net cash a year ago. Cash generated from operations in 1H21 was S$137mn (1H20: S$252mn).

The Negative

– Revenue run rate still weak. After the huge 26% YoY drop in 1H20 revenue, the rebound this year has been weak. 1H21 revenue of S$1.4bn is 22% below pre-COVID 1H19 levels. Life-science and genomics products have yet to reach sufficient scale to drive growth.

Outlook

Venture guided that customer orders remain strong. However, component supplies and operations in Malaysia remain disrupted by lockdowns, creating bottlenecks for the fulfilment of orders.

Maintain NEUTRAL with unchanged TP of S$19.20

Our forecasts are unchanged as we expect stronger revenue momentum in 2H21.

Source: Phillip Capital Research - 10 Aug 2021

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

THE SINGAPOREAN INVESTOR

Investing in Singapore's Hospitality Scene: A Look at the 5 Listed REITs

2

RHB Investment Research Reports

Food Empire - Expanding Ingredients Capability in Vietnam; BUY

3

RHB Investment Research Reports

ST Engineering - Rolling Forward Our Valuation; Reiterate BUY

4

CEO Morning Brief

Singapore Home Sales Set for Worst Year Since Financial Crisis

5

SGX Market Dialogues

Kopi-C With GuocoLand’s Group CEO: ‘We Have Twin Engines for Growth’

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....