Trader Hub

Ascott Residence Trust – Moats on All Sides

traderhub8

Publish date: Thu, 29 Jul 2021, 03:36 PM

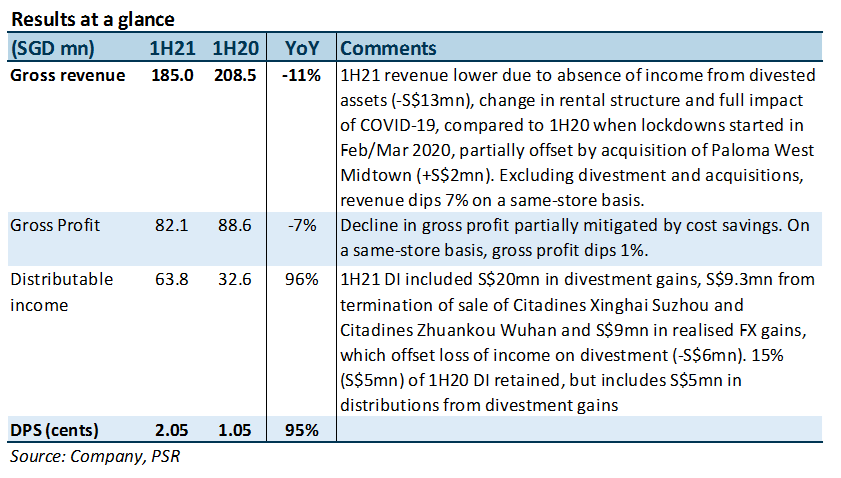

- 1H21 DPU up 95% YoY to 2.05 cents, in line at 47% of our estimate.

- Gradual recovery evident from rising RevPAU, occupancy and better bookings. Redeploying divestment proceeds to higher-yielding investments in extended-stay segment to improve earnings stability and replace divested EBITDA.

- Maintain ACCUMULATE. DDM-based (COE 8.5%) TP raised from S$1.17 to S$1.19. We raise FY21e/22e DPUs by 0.7%/1.2% to capture acquisition of two Sapporo rental housing assets in June. FY23e/24e DPUs raised by 1.8%/2.3% for 45% stake in student accommodation development. ART remains our top pick in the sector. Catalysts include acquisitions and asset recycling. That said, recovery timeline may be more protracted if the virus mutates or there are fresh waves.

The Positives

- Gradual recovery in operations. This was ART’s fourth quarter of RevPAU recovery (Figure 1), led by higher occupancy. 2Q21 RevPAU grew 18% QoQ and 75% YoY. Portfolio occupancy climbed from 50% in 1Q20 to 55% (4Q20: 45%). Recall that 12 properties were closed in 1Q21 due to muted demand. ART reopened eight in May/June and two in July following higher demand. Two properties in Japan remained close but ART continued to receive minimum rent from their master lessees. 1H21 gross profits in China and Australia were up 4% and 103% YoY, supported by higher corporate demand and improvements in their COVID-19 situation. Portfolio also benefitted from block bookings in Australia, Singapore and the US, while two properties in Japan secured group bookings from media groups for the Olympics. Forward bookings have also improved with more corporate and relocation enquiries in the US and Singapore.

- Cost savings. 1H21 revenue was down 11% due to an absence of income from divested assets (-S$13mn), changes in rental structures and the full impact of COVID-19, compared to 1H20 when lockdowns started in February/March 2020. Lower revenue was partially compensated by its acquisition of Paloma West Midtown which contributed S$2mn from 27 February 2021. Digitalisation also reduced man hours and staff costs, resulting in a smaller 7% decline in gross profits. On a same-store basis, revenue and gross profit were down a lesser 8% and 1% respectively.

- Shoring up stable revenue with divestment proceeds. ART has divested six properties since 2020 for S$580mn in proceeds and S$225mn in net gains. Exit yields for these averaged 2%. It has reinvested S$285mn in five long-stay student accommodation and rental housing assets, with an average EBITDA yield of 5%. Four are currently operational and should contribute S$9mn to full-year EBITDA. This will help replace 77.6% of its divested EBITDA. ART’s most recent investment was a 45% stake in a student accommodation in South Carolina, US. The remaining 45%/10% stakes will be held by sponsor Ascott Limited (not listed) and an unnamed US student-housing developer. Construction is scheduled to start in 3Q21 and complete in 2Q23. Development cost is S$146.2mn and EBITDA yield, estimated at 6.2%. The yield is about 120bp higher than its first student accommodation asset, Paloma West Midtown. The latter is a stabilised asset and was acquired on 27 February 2021 at an EBITDA yield of 5%.

The Negative

- Booked S$5.3mn provisions for Park Hotel. ART is in the process of repossessing Park Hotel Clarke Quay after its master lessee failed to make rent payments. On 18 June, it served a letter of demand for the outstanding S$5.9mn after netting off a S$6.8mn security deposit to the guarantor, Park Hotel Management Pte Ltd. Park Hotel Management is currently undergoing liquidation. Park Hotel Clarke Quay has been block-booked by the Singapore government since May 2021 and is expected to be cashflow-positive. ART’s sponsor has been engaged to manage the property while ART assesses its options. Options include bringing in a new master lessee, rebranding under a new hotel operator or divestment. The asset is well-located in Clarke Quay and is expected to benefit from the reopening of international borders as well as a redeveloped Liang Court in 2025. ART is working with liquidators to recover its debt.

Source: Phillip Capital Research - 29 Jul 2021

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trader Hub

CSOP IEdge S-REIT Leaders Index ETF – The Deeper Discounted Singapore REIT ETF

Created by traderhub8 | Jun 12, 2024

Valuetronics Holdings Ltd- Get Paid as Customer Base Is Refreshed

Created by traderhub8 | Jun 03, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

Singapore Post Shares Slide After CEO Fired Over Whistleblower Report

2

3

Johor house best buy

4

CEO Morning Brief

DBS Shares’ 43% Rally Seen Having More Legs as Wealth Fees Rise

5

CEO Morning Brief

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....